Retirement changes the purpose of a portfolio. During your working years, the goal is to build wealth. Once retirement arrives, the goal shifts to generating reliable income.

After more than eight years of retirement, I will share the five lessons that helped me transition from accumulation to income. Whether you're approaching retirement or already there, these lessons may help you avoid a few costly mistakes.

1. There Are More Options Than You Think

Many retirees default to the traditional approach: hold an S&P 500 fund, add bonds, and sell shares when income is needed.

That strategy can work, but it isn't the only option.

I explored dividend growth stocks, real estate, bonds, and eventually high-yield income investments. Today, my portfolio yields roughly 11.5%, allowing me to spend a portion of the income while reinvesting the rest.

The biggest takeaway is not that everyone should copy my approach. It's that retirees should explore multiple income strategies before deciding what fits their goals and risk tolerance.

2. Start Income Investing Earlier

One thing I would change is the timing of my transition.

I waited until retirement to sell growth investments and build an income portfolio. Looking back, I would have started one or two years earlier.

Doing so would have reduced sequence-of-returns risk and provided more time to learn income-focused asset classes such as BDCs, preferred shares, closed-end funds, and covered call ETFs.

3. CNBC Isn't Research

Financial television is entertaining, but most headlines have little impact on long-term retirement income.

Rather than reacting to inflation reports, Federal Reserve meetings, or daily market moves, I focused on researching investments that can consistently generate income.

That research comes from investment analysis, newsletters, investor communities, and conversations with other experienced investors.

4. Plan for Price Corrections

One of the biggest mindset shifts in retirement is learning to welcome price declines.

When I buy an investment today, I already have a plan if the price falls: buy more.

As long as the underlying business remains healthy and the income stream is intact, lower prices can actually improve future income by increasing yield on new purchases.

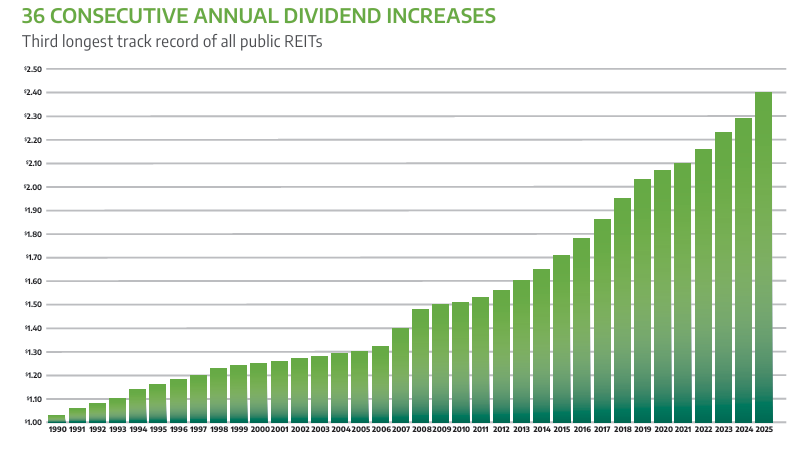

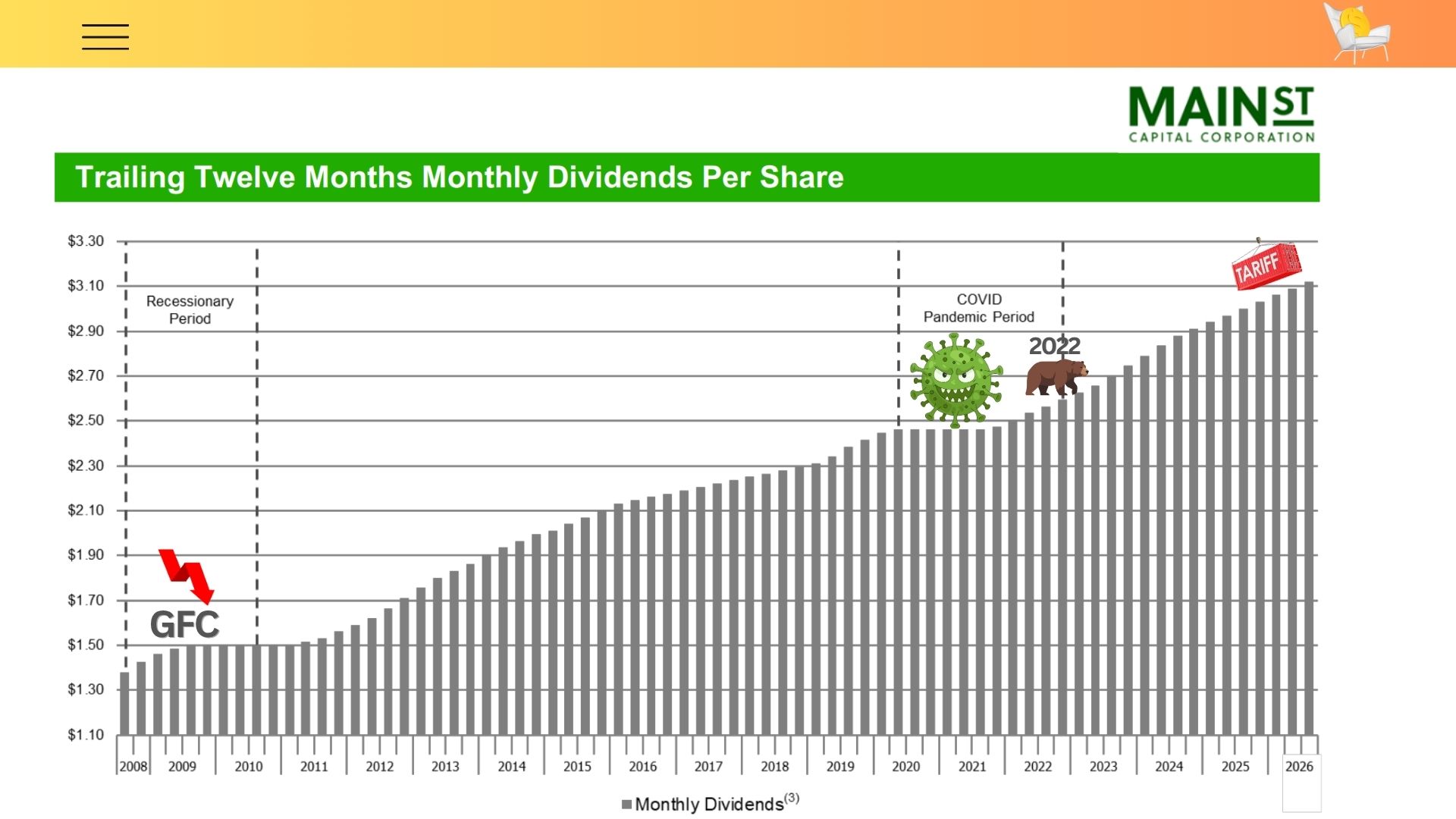

MAIN Street Capital is one example. While some investors worry about short-term price weakness, I focus on the company's ability to continue generating reliable distributions.

5. Don't Go Alone

The final lesson is simple: investing is easier when ideas are shared.

Many of my best investment ideas came from other investors rather than my own independent research. Discussions about funds, dividends, and portfolio construction often uncover opportunities that would otherwise be missed.

Whether through online communities (including the Armchair Insider Lounge), articles, or investor groups, surrounding yourself with like-minded investors can dramatically improve the learning process.

My Take

There is no perfect retirement strategy. Some investors will prefer growth. Others will prioritize income. Many will choose a blend of both.

The key lessons are simple: explore more options, start preparing before retirement arrives, focus on research instead of headlines, embrace corrections as opportunities, and learn from other investors.

Retirement isn't just about building a portfolio. It's about building an income stream that can support the life you want to live.

To learn more, click here for the full Review.

Want to see how these funds fit into a real-world retirement strategy? I share my full portfolio and monthly updates for free, here: Armchair Insider. If you want to learn from other Income Investors (I do!), check out the Armchair Insider Lounge.