There’s been an explosion of new income funds offering 8%+ yields. The problem? Most haven’t been tested in a real recession.

The Global Financial Crisis was the ultimate stress test. Prices collapsed. Credit froze. Dividends were slashed across corporate America.

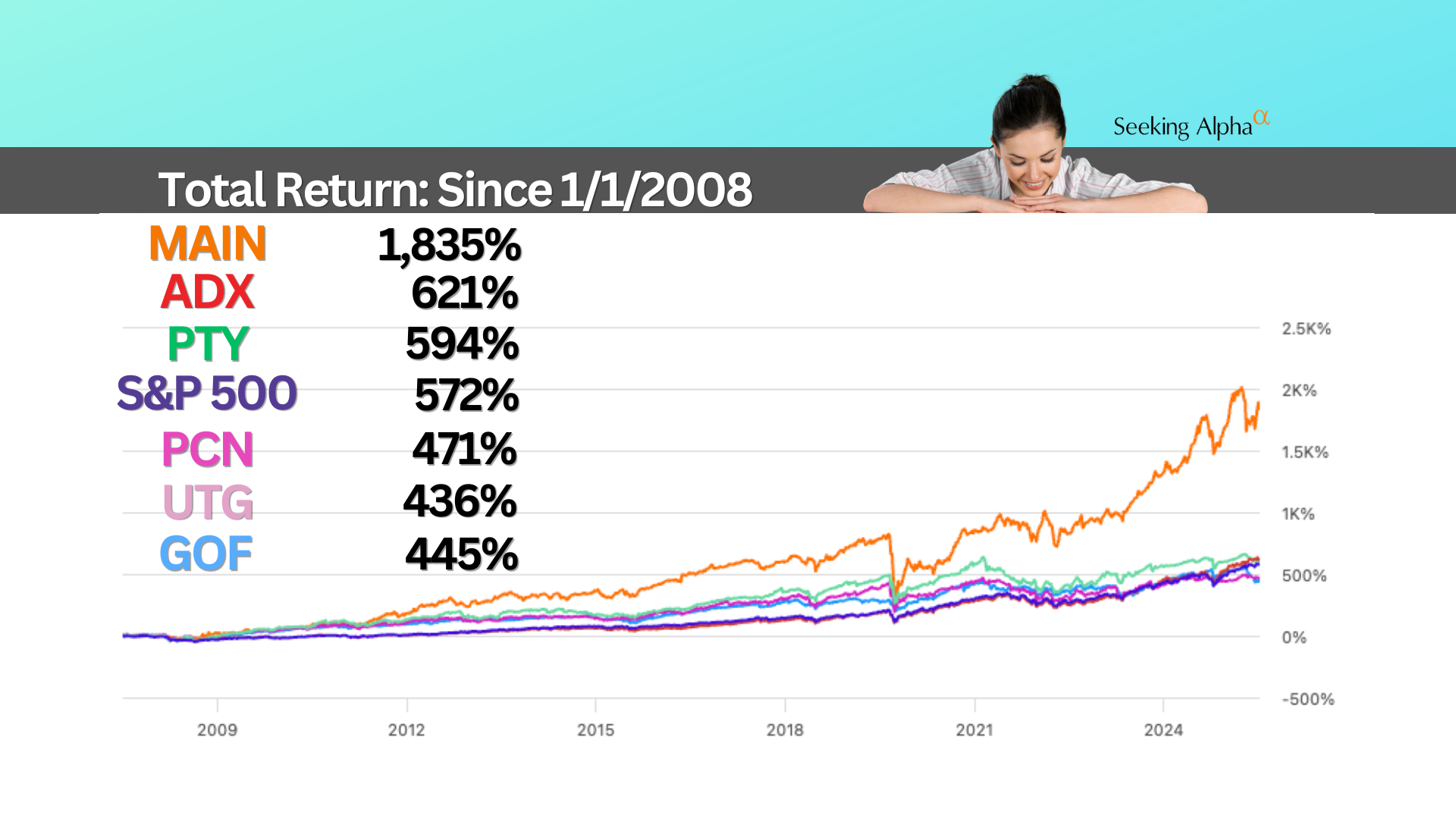

Today we’re looking at six income investments whose histories go back before 2008. Five maintained their distributions during the crisis. One reduced payouts temporarily but delivered strong recovery returns. I currently hold five of the six.

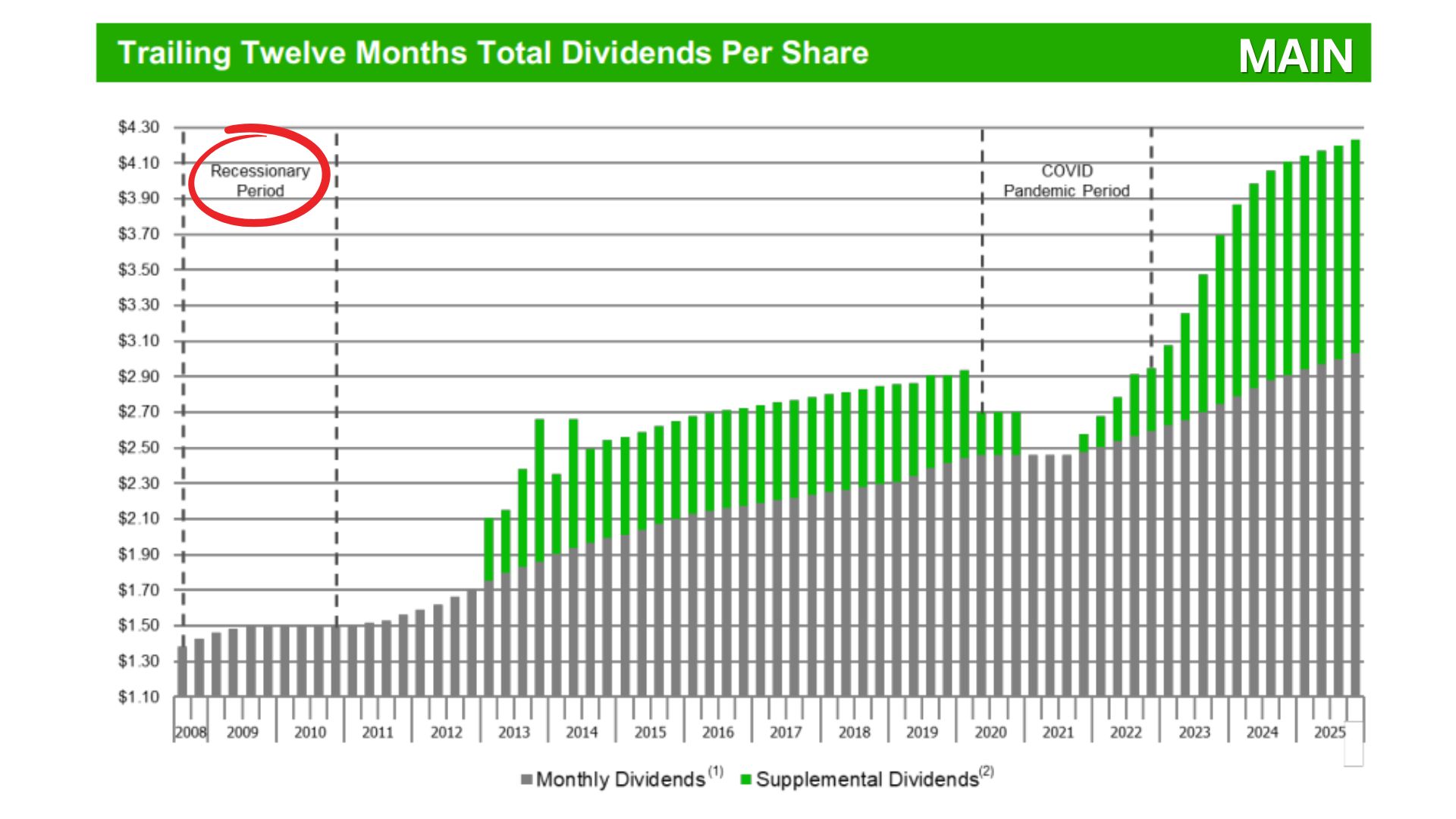

MAIN – Income and Growth

Main Street Capital yields about 5.2% on regular dividends, or roughly 7.2% including supplemental payouts.

The remarkable part is not the yield. It’s the consistency.

MAIN did not cut its regular dividend during 2008. Not once. And since 2007, the dividend has steadily increased.

Unlike most income investments, MAIN delivered both dividend growth and long-term price gains. That performance explains why it trades at a premium to NAV, often near 1.8x.

It’s rarely cheap. History suggests dips are opportunities.

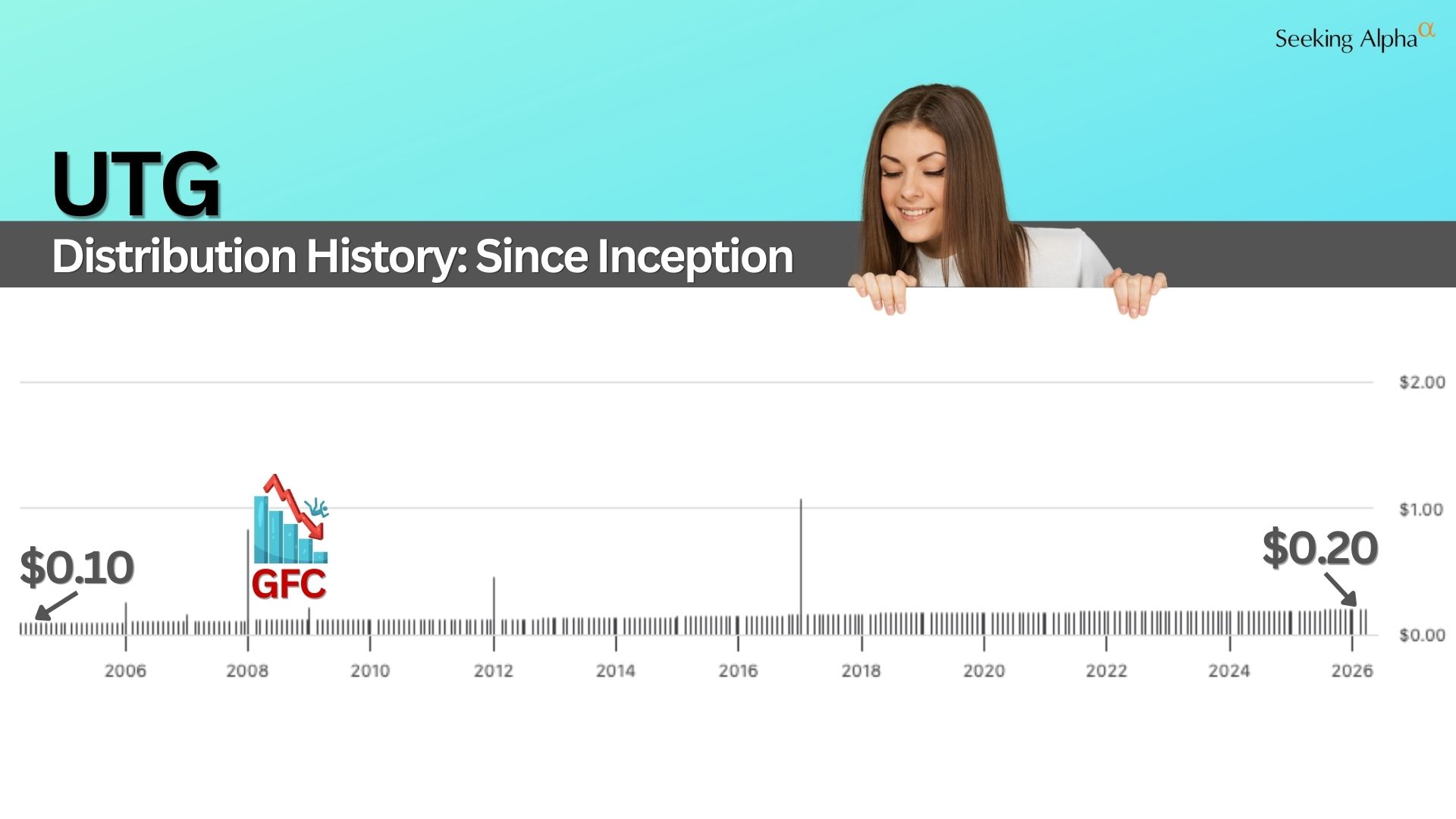

UTG – Utilities That Held Steady

Reaves Utility Income Trust currently yields about 6.6%. During the GFC, the price fell. The income did not.

UTG generates income from stock dividends, capital gains, leverage, and covered calls. The yield has fallen from prior highs near 10% because price appreciation has been strong.

It’s a reminder that lower yield sometimes reflects stronger performance.

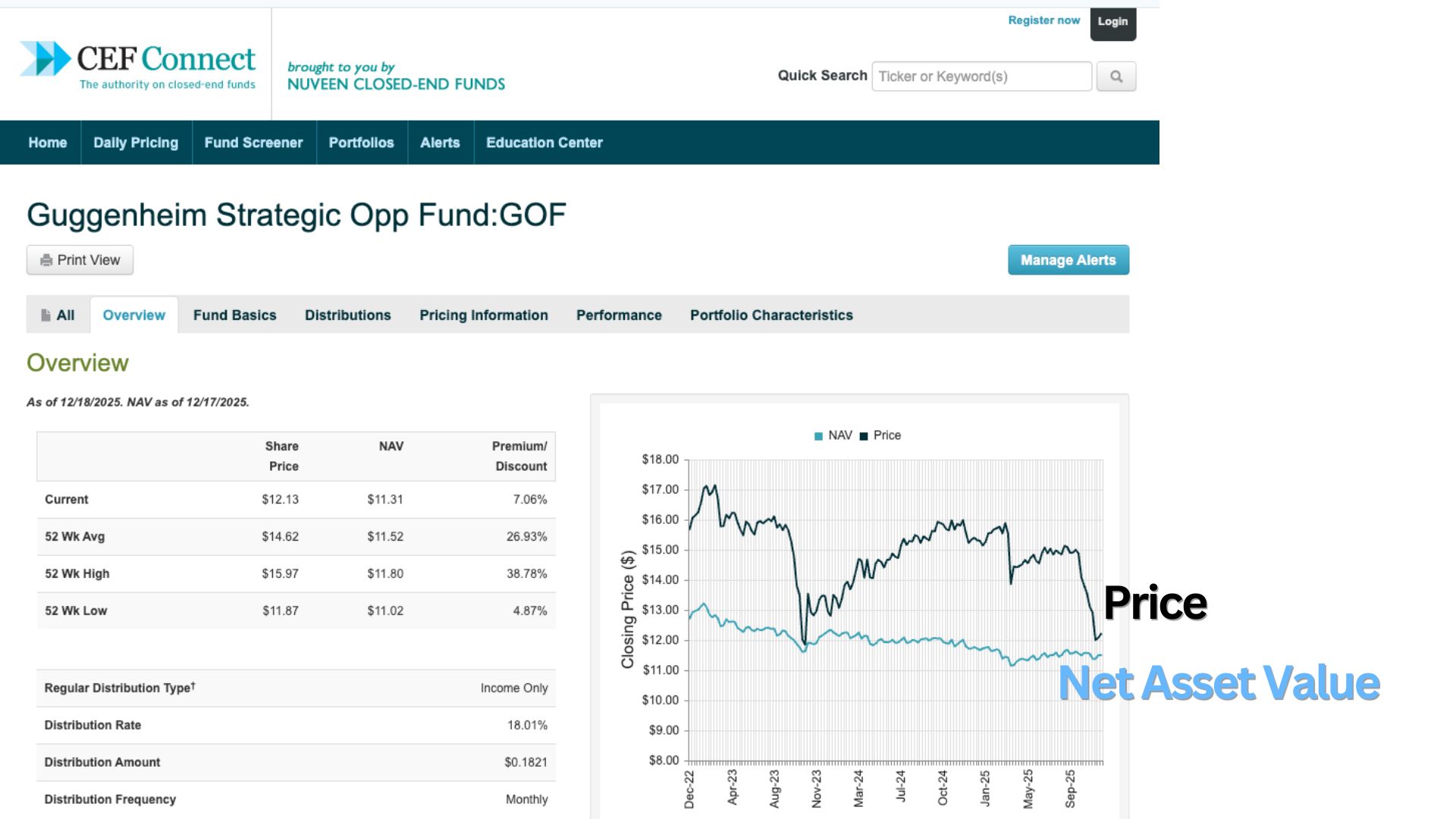

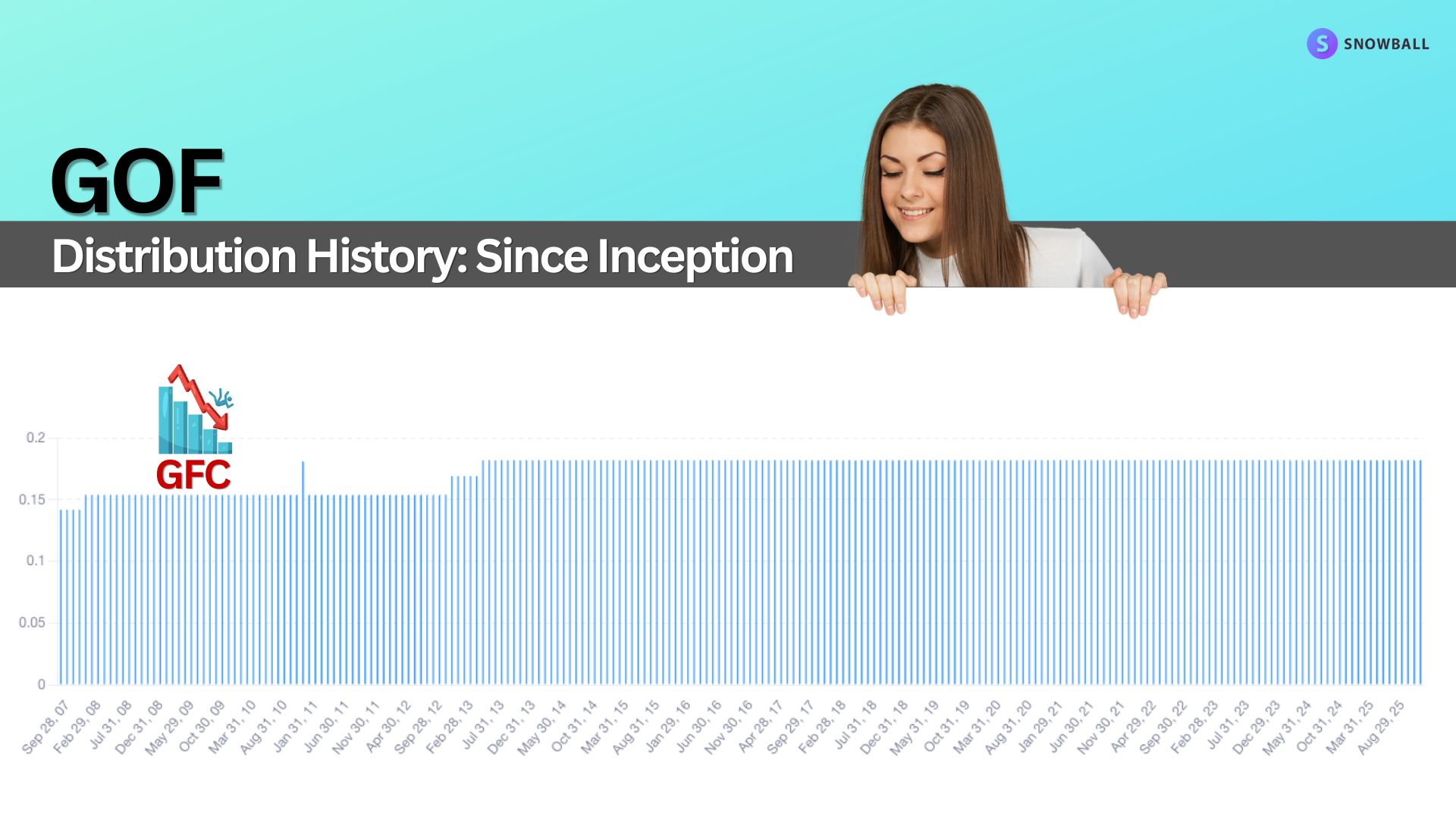

GOF – High Yield, Premium Risk

GOF yields roughly 18%. The distribution history appears extremely stable, even through 2008.

But price and NAV tell a more complicated story.

GOF often trades 20–25% above NAV. Returns depend heavily on when you buy. It holds over 1,400 credit-related securities, uses leverage, and sells options.

At large premiums, I consider it high risk. As the premium compresses, it becomes more attractive.

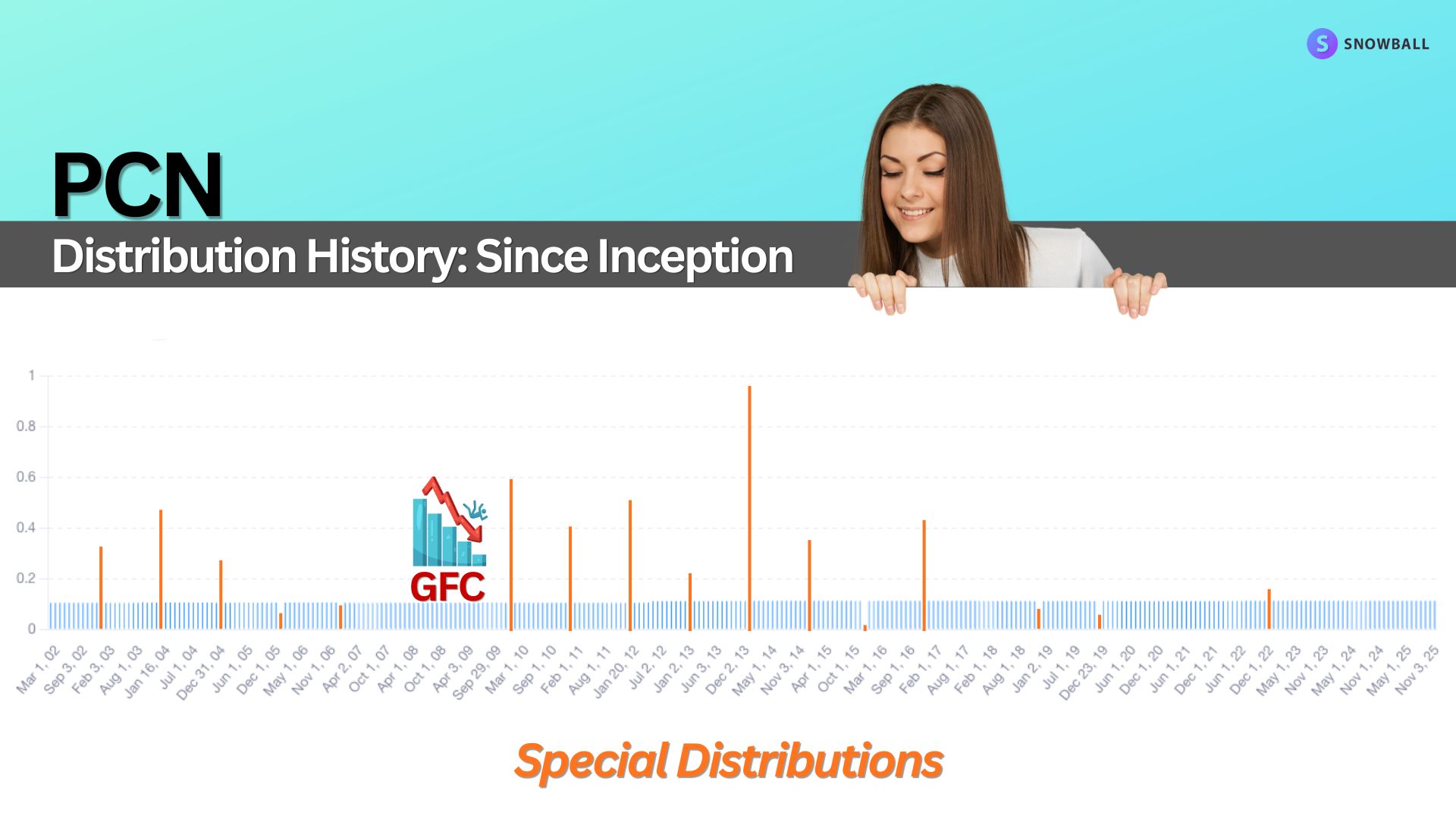

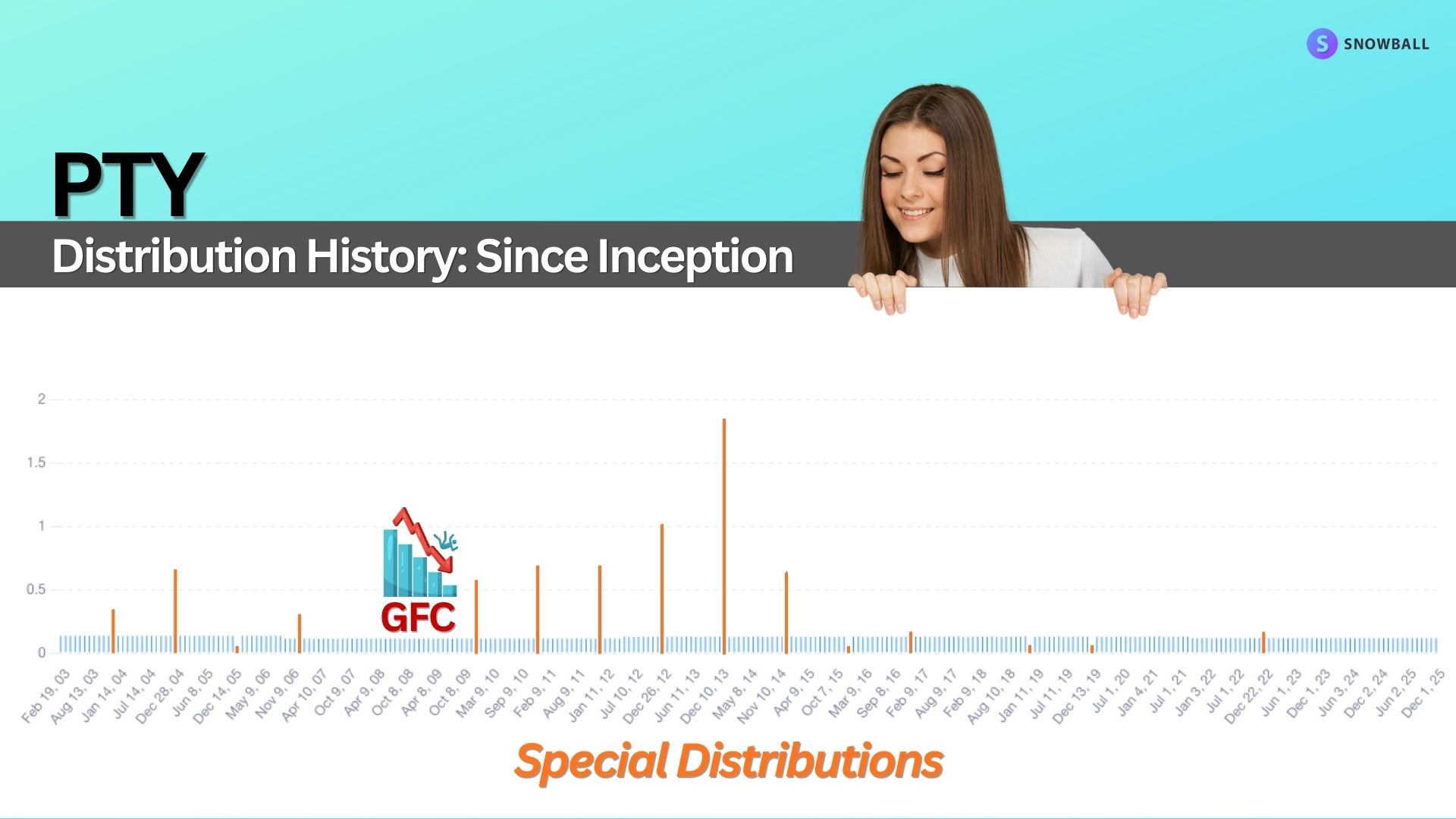

PCN & PTY – Pimco Credit Survivors

PCN and PTY yield around 10–11%.

PCN has maintained an $0.11 monthly distribution since 2002, excluding specials. PTY’s payout has never dropped below $0.115, even during 2008–2009. PTY even paid a special distribution in 2009.

Both rely heavily on active credit management and trade at premiums or discounts depending on sentiment.

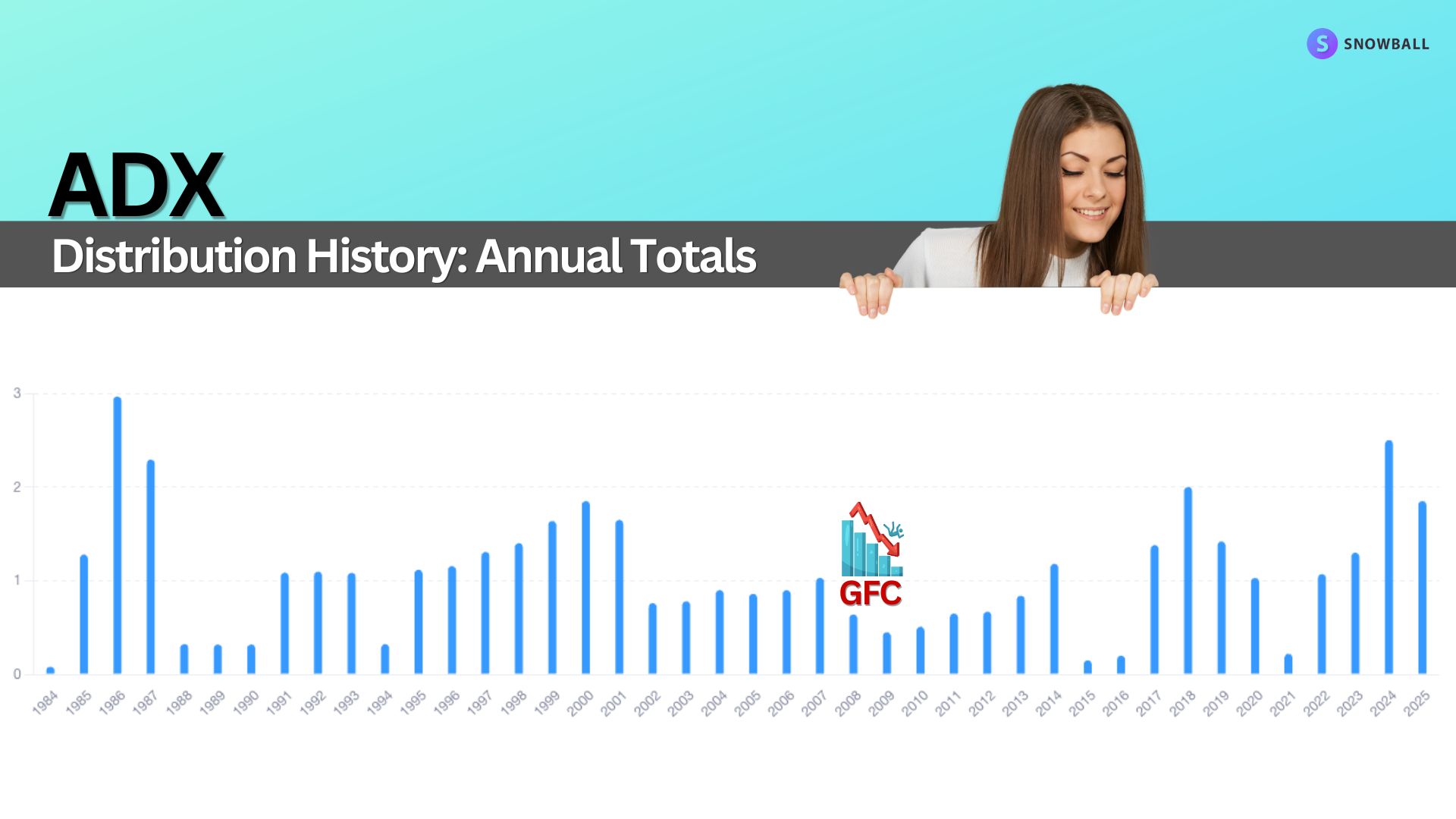

ADX – Variable Income, Strong Returns

ADX targets distributing 8% of NAV annually, so payouts fluctuate.

In 2009, distributions dipped. But ADX rebounded sharply, delivering a 27% total return that year and long-term outperformance versus the S&P 500.

Most income funds sacrifice growth. ADX has delivered both.

My Take

Five of these six funds made no distribution changes during the worst financial crisis in decades. ADX adjusted payouts but compensated through appreciation.

Since January 1, 2008, three of the six have actually outpaced the S&P 500.

New high-yield funds may look attractive. But durability matters.

To learn more, click here for the full Review.

Want to see how these funds fit into a real-world retirement strategy? I share my full portfolio and monthly updates for free, here: Armchair Insider. If you want to learn from other Income Investors (I do!), check out the Armchair Insider Lounge.