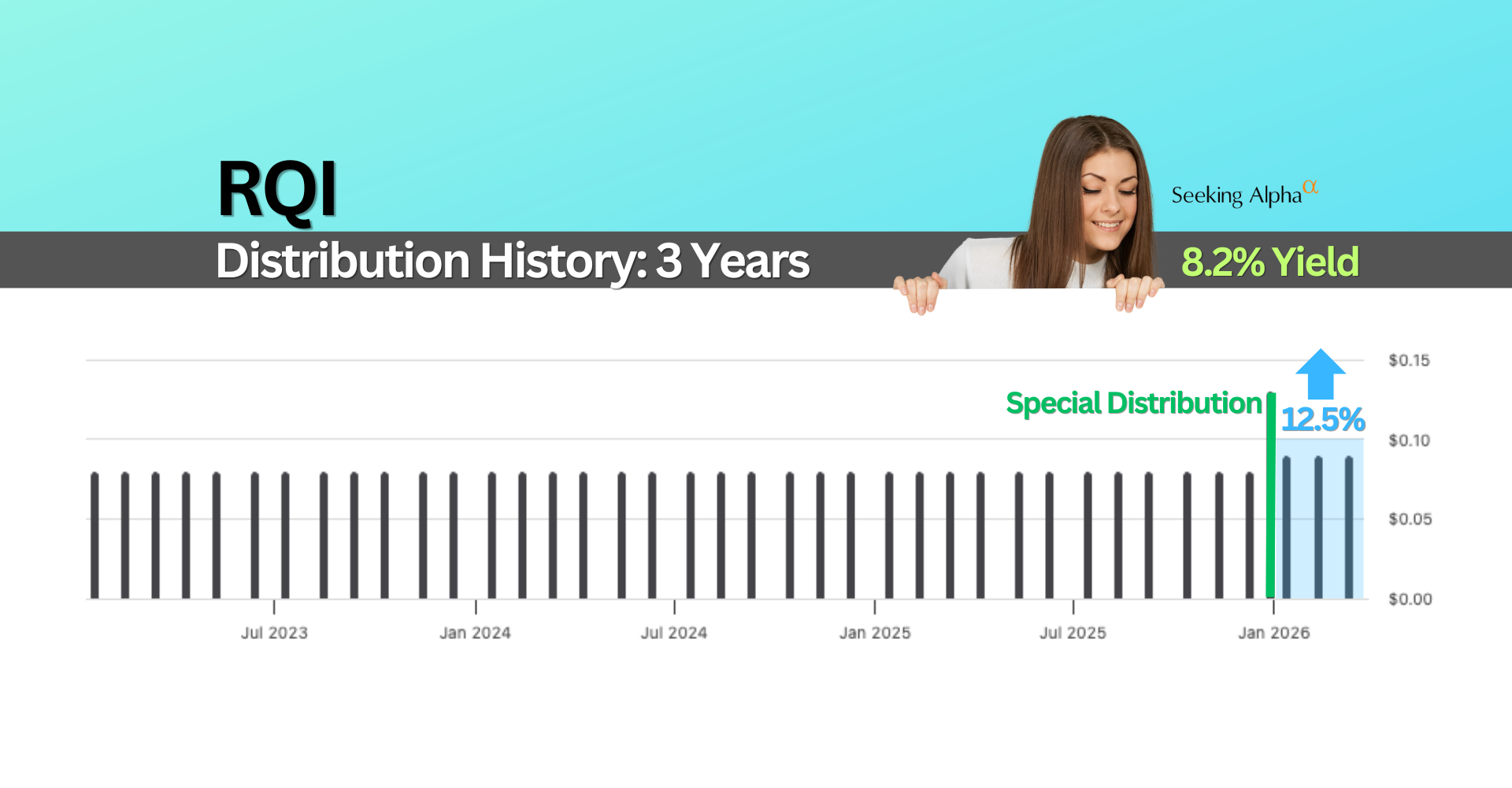

After a lackluster year for real estate, investors in Cohen & Steers Quality Realty Income Fund (RQI) received a welcome surprise: a $0.13 special distribution on top of the regular payout. Even better, management announced a 12.5% increase in the regular monthly distribution.

RQI now yields about 8.2%, trades at a modest discount to net asset value, and has regained attention from income investors. Let’s take a look under the hood.

A 20+ Year Distribution Record

RQI’s distribution history stretches back more than two decades. Before the 2008 financial crisis, the fund paid generous special distributions. Then real estate collapsed.

Distributions fell dramatically — from the equivalent of $0.45 per quarter down to $0.09 per quarter, an 80% decline. If you believe we’re heading into another 2008-style real estate meltdown, this likely isn’t the right fund for you.

Since 2009, however, income has been consistent. No reductions. Several increases.

Quarterly payouts climbed from $0.09 in 2009 to $0.24 by 2015–16. The later shift back to monthly distributions at $0.08 per month looked like a cut on charts, but it wasn’t. It was equivalent on an annual basis.

Now in 2026, the payout has increased again to $0.09 per month. The quoted 8.2% yield does not include the recent special distribution. That was a bonus.

What Is RQI?

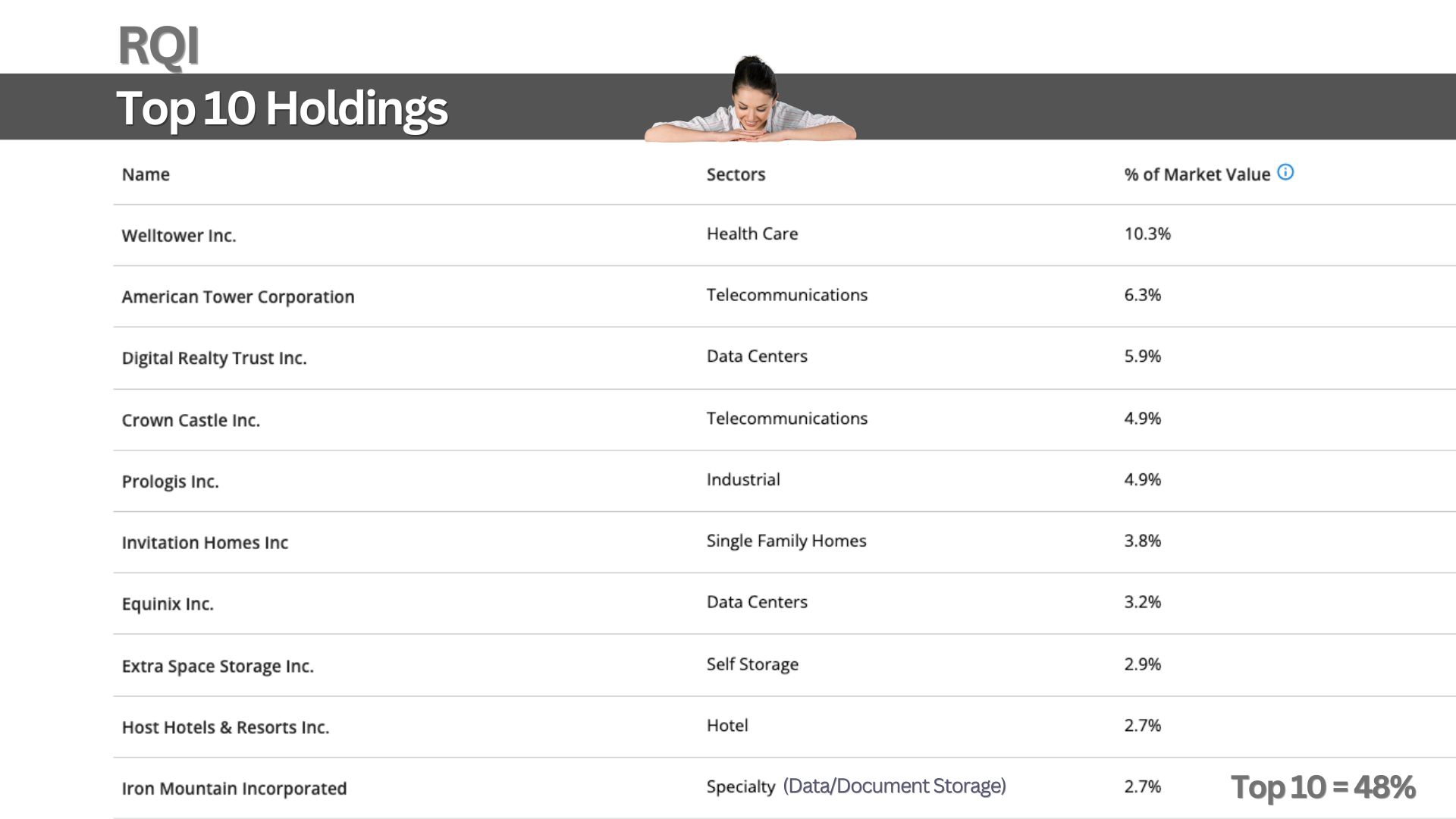

RQI is a closed-end fund focused on real estate companies and REITs. It holds over 200 positions, but it is top-heavy: the top 10 account for roughly 48% of assets.

The largest holding is Welltower, a senior housing REIT that delivered strong performance recently. Another major position is American Tower, a global cell tower operator. Many of the largest holdings are established S&P 500 companies.

Beyond common REITs, about 18% of the portfolio includes preferred shares and corporate bonds. These typically provide steadier income and less volatility.

The portfolio generates income, but not enough to fully cover a 8%+ yield. The remainder comes from realized gains — profits from actively trading holdings. In strong markets, that works well. In weaker markets, return of capital may be used to maintain consistent distributions.

Taxes, Fees & Competition

For 2024, most of RQI’s distributions were classified as capital gains, which are generally more tax-efficient than ordinary income. There was also some Section 199A income. No return of capital was reported for that year.

Fees are the trade-off. The management fee is about 1.11%, plus borrowing costs from leverage. Like most closed-end funds, it’s not cheap.

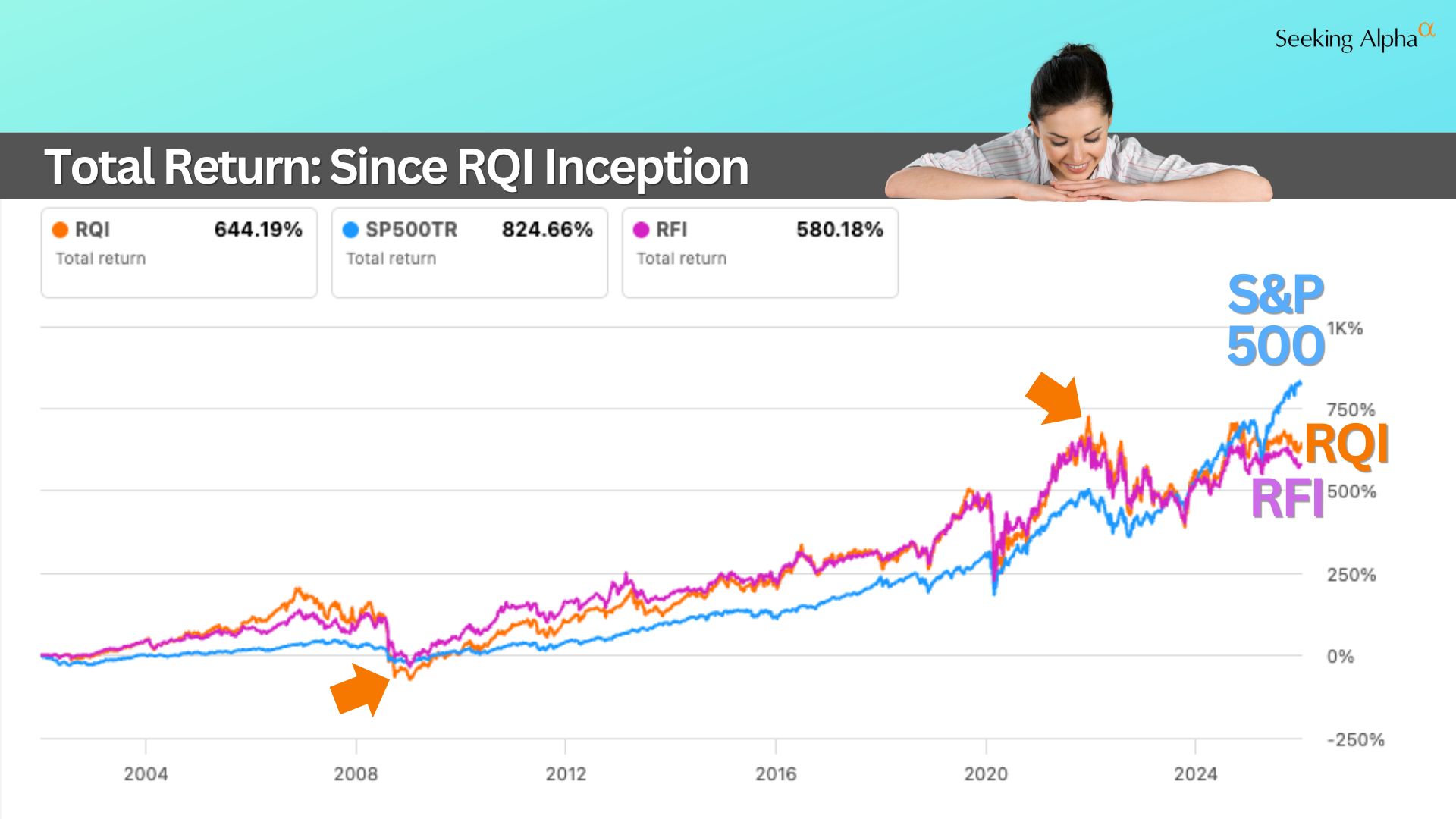

RQI’s sister fund, RFI, offers similar exposure without leverage. Over time, leverage has amplified both gains and losses.

My Take

Real estate funds are sensitive to interest rates. Rising rates can pressure prices. Outside of extreme events like 2008, however, the income has been relatively steady.

I keep 5–10% of my portfolio allocated to real estate funds, including RQI. The recent distribution increase makes it more attractive at current pricing.

To learn more about RQI’s distribution increase, leverage strategy, competitors, and valuation discount, watch the full video breakdown linked here.

Want to see how these funds fit into a real-world retirement strategy? I share my full portfolio and monthly updates for free, here: Armchair Insider. If you want to learn from other Income Investors (I do!), check out the Armchair Insider Lounge.