More than 70 years have passed since the publication of the works that became the foundation of the Modern Portfolio Theory by Markowitz, Sharpe, and Miller. It has been over 35 years since the authors were awarded the Nobel Prize in Economics. This theory shows how to construct the optimal investment portfolio from available assets. Over the years, it has been scrutinized inside and out and has gone mainstream as the source of basic investment principles – "don't put all your eggs in one basket." In terms of practical benefit, the investment consensus was that the theory works "in the very long term," and that one cannot make quick money with it. The theory found its application mainly on the pages of textbooks and library shelves.

The main problem with the practical application of Modern Portfolio Theory is that it deals with the expected (future) returns of the assets from which the portfolio is to be composed. How can one apply the theory in practice if we don't know its main parameters? However, this is also its genius – it can never be replaced by artificial intelligence, which will never be able to predict the future. But can Modern Portfolio Theory be used in practice over shorter periods? It turns out, yes.

As noted, the most important factor for the successful application of Modern Portfolio Theory is the correct estimation of the expected returns of assets. This can be done using a probabilistic model. But if a security falls or rises sharply in a certain period, we understand that a period of correction and reverse movement is likely to occur. Therefore, the second principle for successfully applying Markowitz's theory is regular rebalancing of the portfolio to a new optimal structure, taking into account the dynamics of the portfolio's assets over the past period.

But there is a third principle – Markowitz's theory is very difficult to apply in practice to assets whose return distribution differs significantly from the Normal (Gaussian) distribution. This applies to almost all individual securities that carry individual (or specific) risks. The solution is to work with indices, which, due to the large number of constituent instruments, neutralize specific risk, leaving only market risk. The dynamics of an index are much more "normalized," and an index, unlike an individual security, cannot sharply rise or fall and remain in that state for a long time. An index will necessarily correct after such movements, justifying the need for regular portfolio rebalancing.

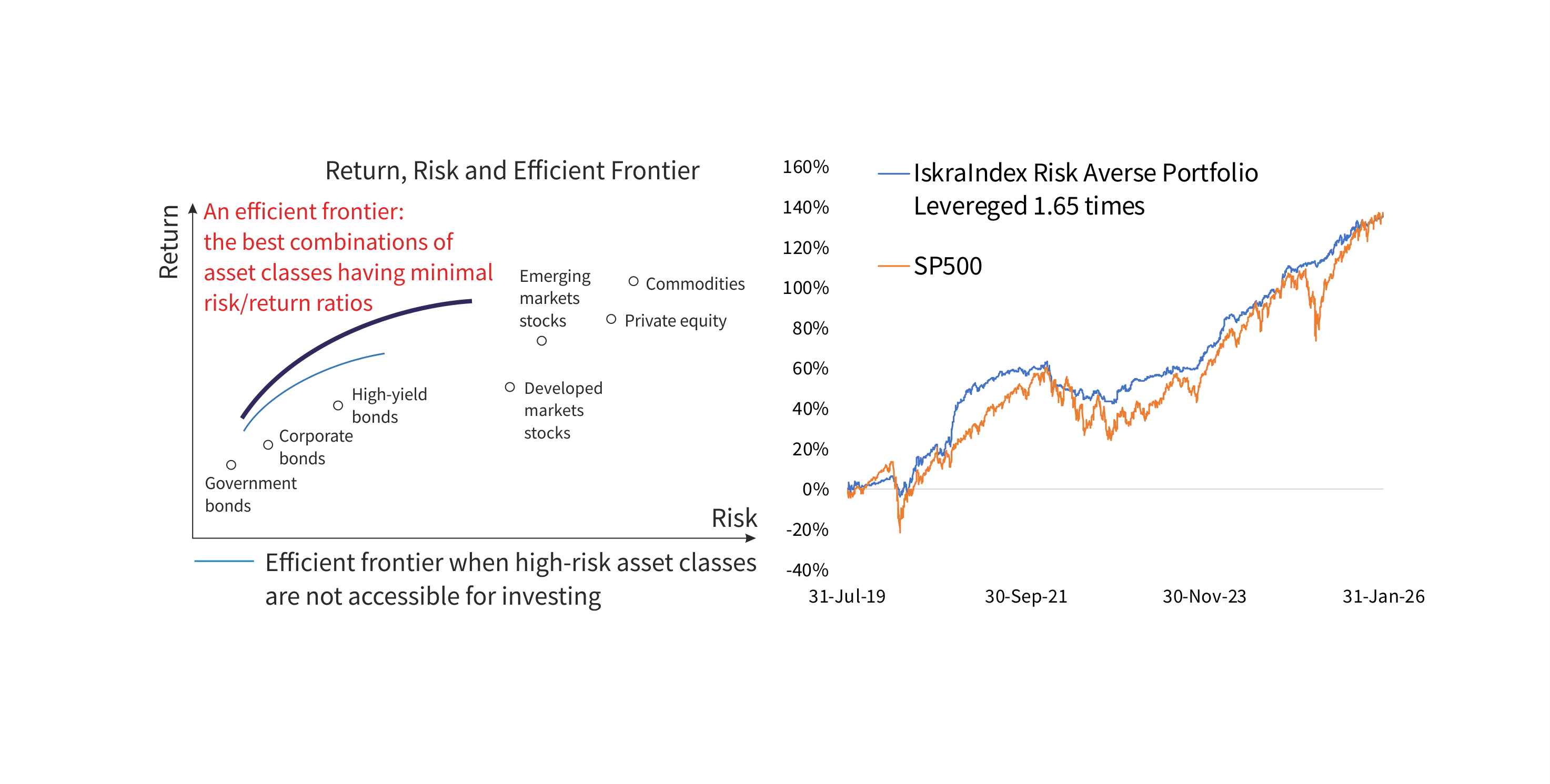

An optimal portfolio, constructed based on the principles of modern portfolio theory, is particularly effective for low and medium-risk portfolios. This is because carefully "mixing" a small portion of higher-risk instruments into a conservative portfolio allows shifting the efficient frontier of the set of portfolios to the right and upward, beyond which no possible combinations of the instruments included in the portfolio exist.

Furthermore, if you have access to a portfolio with a low risk level and a return not inferior to the benchmark, you can lever this portfolio. By doing so, you match the benchmark's risk level while significantly exceeding its return. This is another practical solution enabled by Modern Theory.

In the public domain on Snowball-Analytics, you can view the index portfolio IskraIndex Risk Averse (https://snowball-analytics.com/public/portfolios/omiemuxndmtcodwhmpyx). It is composed of the largest index ETFs and utilizes all the principles described above. Leveraged 1.65 times, this portfolio is ready to be significantly less risky alternative to an investment in S&P500 Index.