If you have the prerequisite minimum level of knowledge, I often recommend that people try to manage their own money. While the world of finance can seem intimidating, the math behind "Do It Yourself" (DIY) investing is compelling—specifically when you look at the destructive power of fees.

To understand why, we have to look at the data. One of the best resources for this is the SPIVA (S&P Indices Versus Active) Scorecard. As of the time of this writing, here is the data over the last 15 years regarding U.S. Large-Cap funds:

88.29% of funds underperformed the S&P 500

11.71% of funds outperformed the S&P 500

Why are the vast majority of professional funds underperforming the S&P? It is rarely a lack of skill; it is almost always a result of fees.

Different funds have different fee structures, but it is common to see a minimum fee of at least 1% of the portfolio value annually, sometimes rising higher than 2%. When you are compounding interest over a long period, that small percentage makes a massive difference.

The Math of Fees

Let’s make an extreme, simplified assumption. Say that over a 30-year period, the S&P 500 has a return of 8% annually.

Now, let’s say you invest in an actively managed fund that actually beats the S&P 500’s performance regarding pure asset selection, achieving 9% returns each year. However, this fund charges a fee on assets under management of 2% annually, meaning your return after fees is only 7% annually.

Imagine you invested $100,000 in the S&P 500 (through a low-cost ETF like SPY) at the beginning of the 30 years, and another $100,000 in the active fund.

Even though the fund employees were skillful and made choices that outperformed the S&P 500 pre-fee, here is where you end up:

The Active Fund (7% net return):

$100,000 *(1.07)^(30) = $761,225.50

The S&P 500 DIY Portfolio (8% return):

$100,000 *(1.08)^(30) = $1,006,265.69

The Difference:

$245,040.19

In this simplified example, the investor ended up with nearly a quarter-million dollars more in the DIY portfolio. This is the "fee drag" in action.

Looking at the SPIVA data, we can see in hindsight that for 11.71% of funds, the investor would have been better off paying the fees for that outperformance. But how do you know if the fund you are choosing today is one of the lucky 11.71% that will win over the next 15 years? The odds are not in your favor.

I do not want to oversimplify this; there are many good funds and skillful money managers out there. However, based on the math I have seen, I personally manage my own portfolio to avoid these fees. When choosing ETFs to put in my portfolio, I specifically look for passively managed ones with low expense ratios.

The Right Tools for the Job

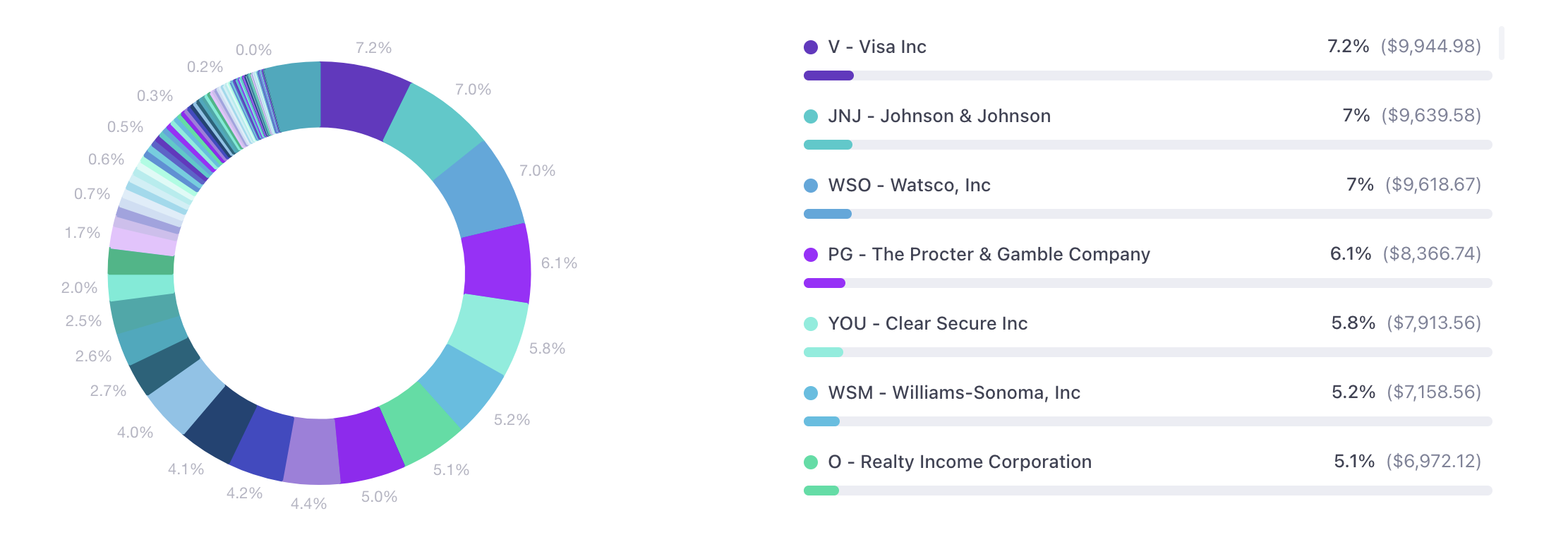

If you are going to go the DIY route to save on fees, you need to treat your portfolio with the same seriousness that a professional manager would. That means knowing exactly how your asset allocation looks, tracking your dividends, and benchmarking your performance to ensure you are actually capturing those market returns.

As a DIY investor, it is helpful to have powerful tools to guide your decision-making. I have personally found Snowball Analytics to be a very valuable tool for a guy like myself. It allows me to automate my portfolio tracking, analyze my diversification, and see my true annualized returns net of any costs.

If you want to upgrade your toolkit, we are running a special New Year sale on Snowball Analytics from December 22 to January 1.

Click here to get 30% OFF Snowball Analytics until January 1

Be sure to use the promocode: ryan

Managing your own money doesn't mean you have to do it without support. By cutting out high management fees and using high-quality analytics tools, you put yourself in the best position to let compound interest work for you, not a fund manager.

Claim your 30% discount on Snowball Analytics here

Disclaimer: The following content is for educational purposes only and does not constitute financial advice. All investments carry risk, and you should perform your own due diligence or consult a certified professional before making investment decisions.

Ryan O'Connell, CFA, FRM