Most income investors want the same combination:

Consistent income, strong long-term returns, and a good entry price.

The problem? High-quality investments are rarely cheap.

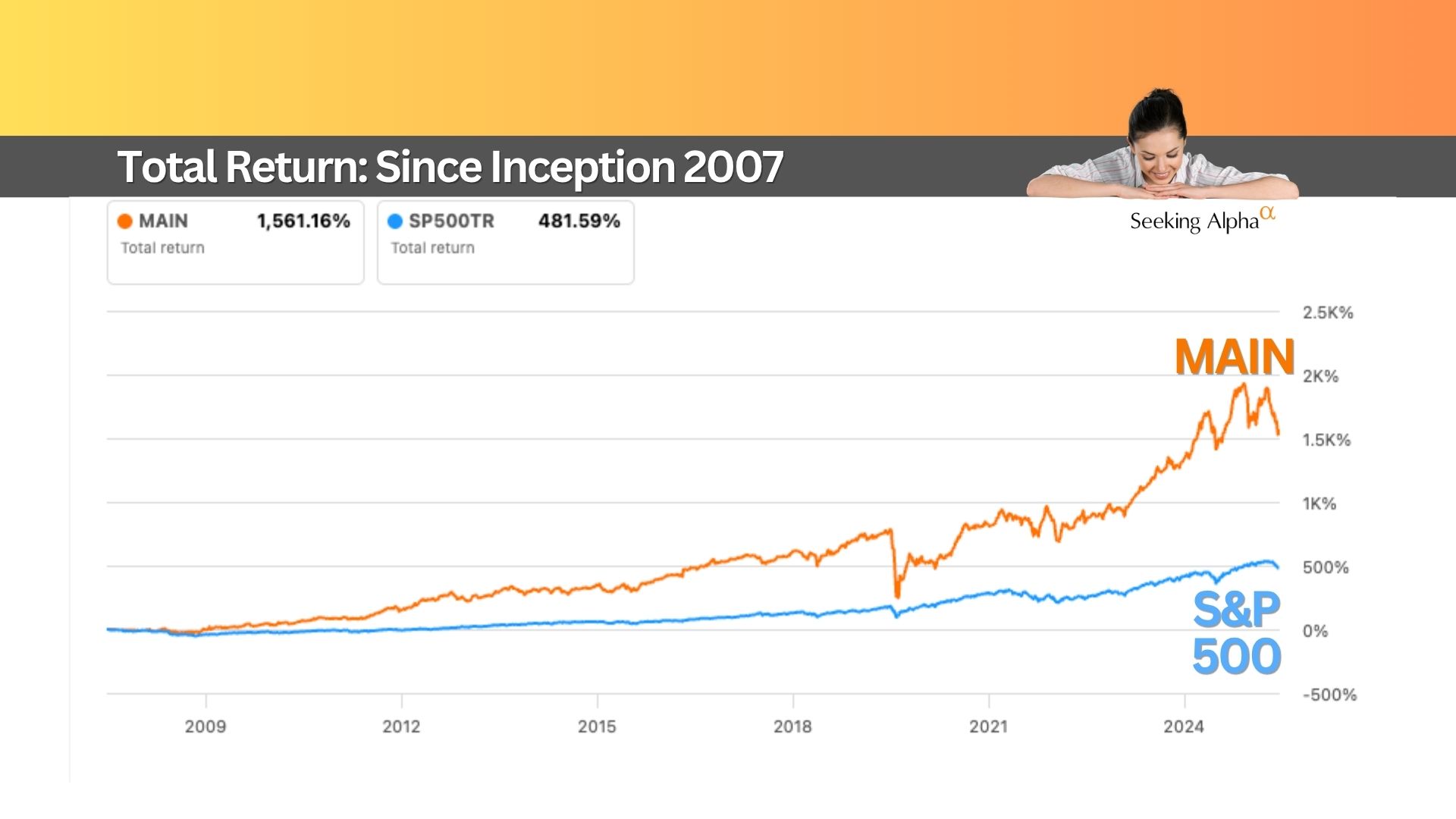

That’s why Main Street Capital Corporation has been on my watchlist for years. It’s one of the best Business Development Companies (BDCs) in the market—but almost always trades at a premium.

Now that the price has pulled back, the question becomes:

Is this just noise… or a real opportunity?

One of the Best Income Track Records

Let’s start with what matters most: income.

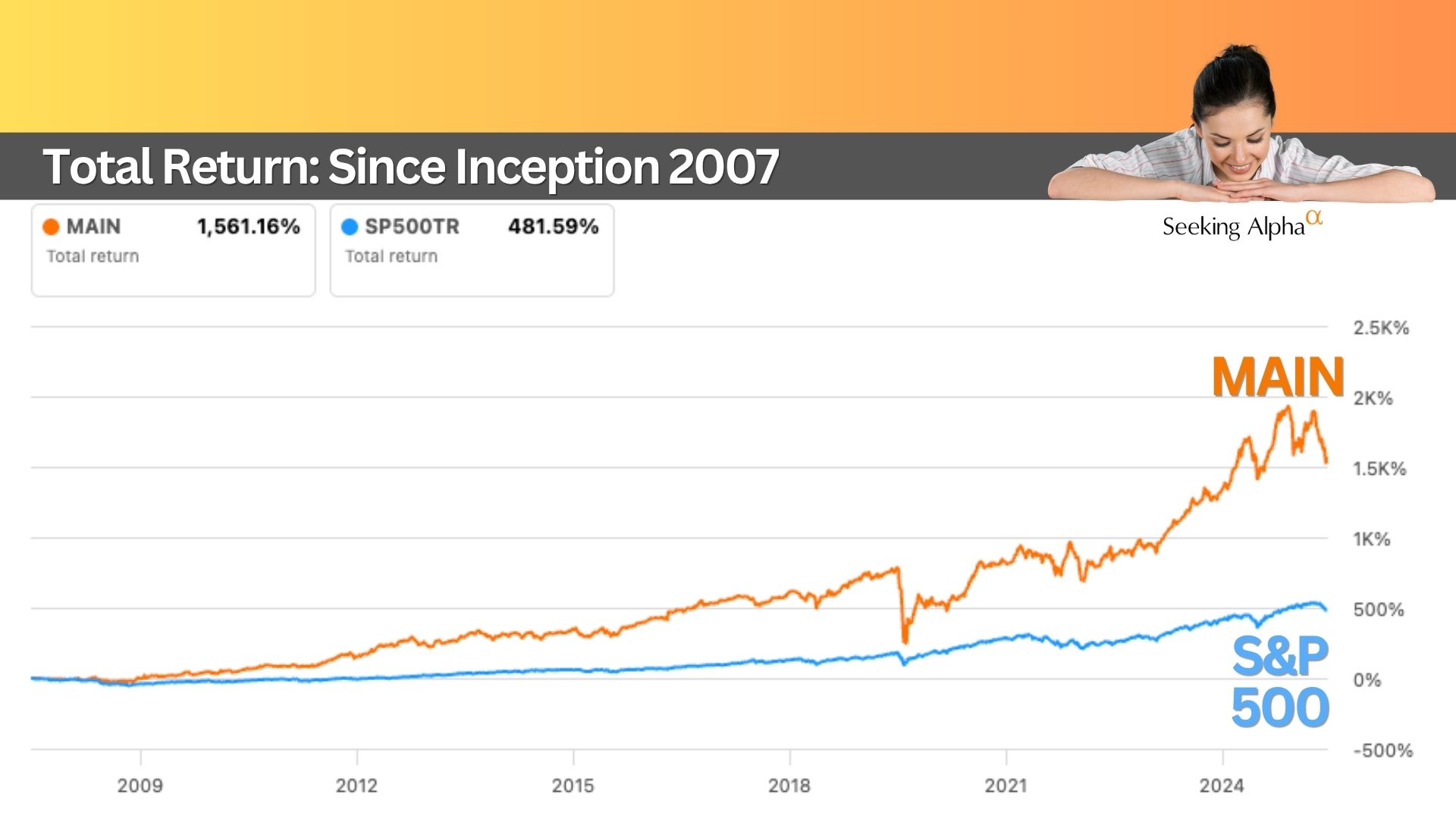

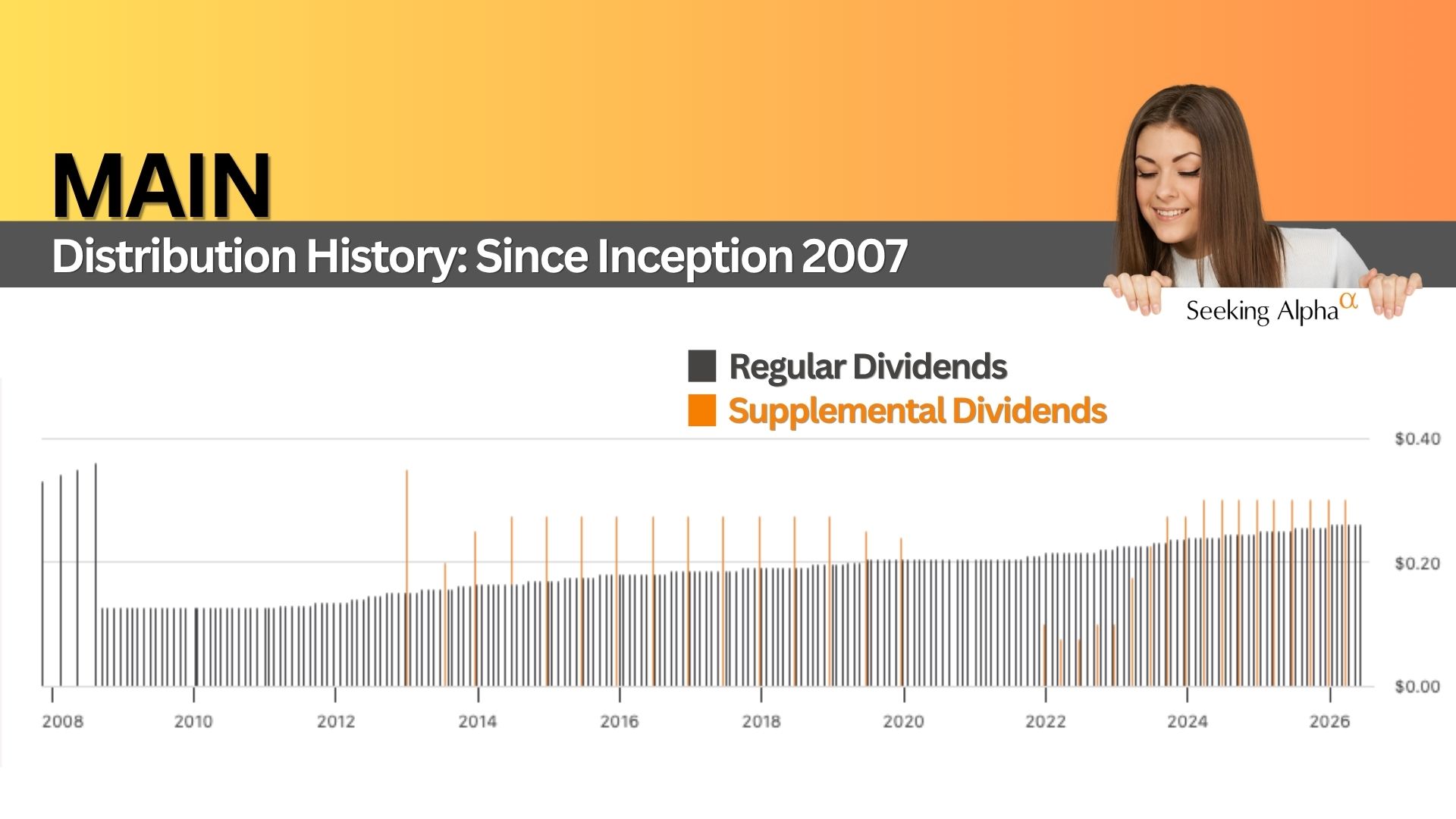

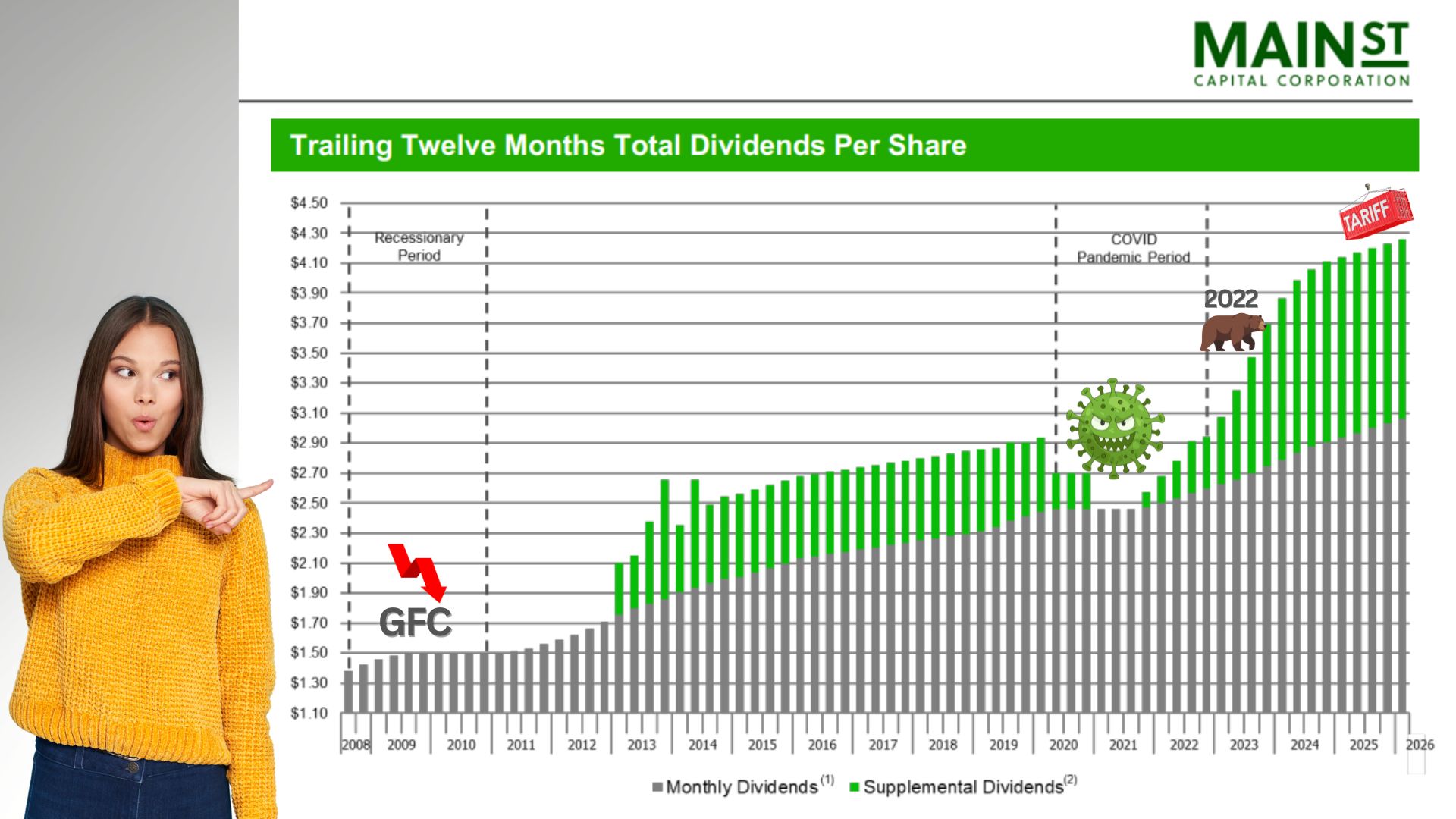

MAIN has one of the strongest distribution histories in the entire BDC space. But it’s slightly more complex than most.

It pays:

Regular dividends (stable, predictable)

Supplemental dividends (variable, performance-driven)

Management sets the regular dividend at a level they believe can survive any environment—recessions, rate changes, or economic slowdowns.

Supplemental dividends are the upside.

That structure has delivered something rare: nearly two decades without a cut to the regular dividend.

How MAIN Generates Income

MAIN is a Business Development Company that lends to middle-market businesses—but with more flexibility than a traditional bank.

Its income comes from four main sources:

Interest and loan fees

Dividends from equity investments

Realized gains from selling equity stakes

Management fees from external funds

The key differentiator is equity exposure.

MAIN allocates roughly 30% to equity, compared to a BDC average closer to 6%. That introduces more upside potential—and historically, it has paid off.

Income Through Different Market Cycles

Even during events like the Global Financial Crisis and COVID, the core dividend remained intact.

That level of consistency is why investors are willing to pay a premium.

Risks to Watch

Two concerns often come up:

AI / software exposure:

Minimal. Only about 4% exposure, with most loans secured in first-lien positions.

Interest rates:

Lower rates can pressure income, but MAIN has offset this through diversified revenue streams. Net investment income still increased in 2025.

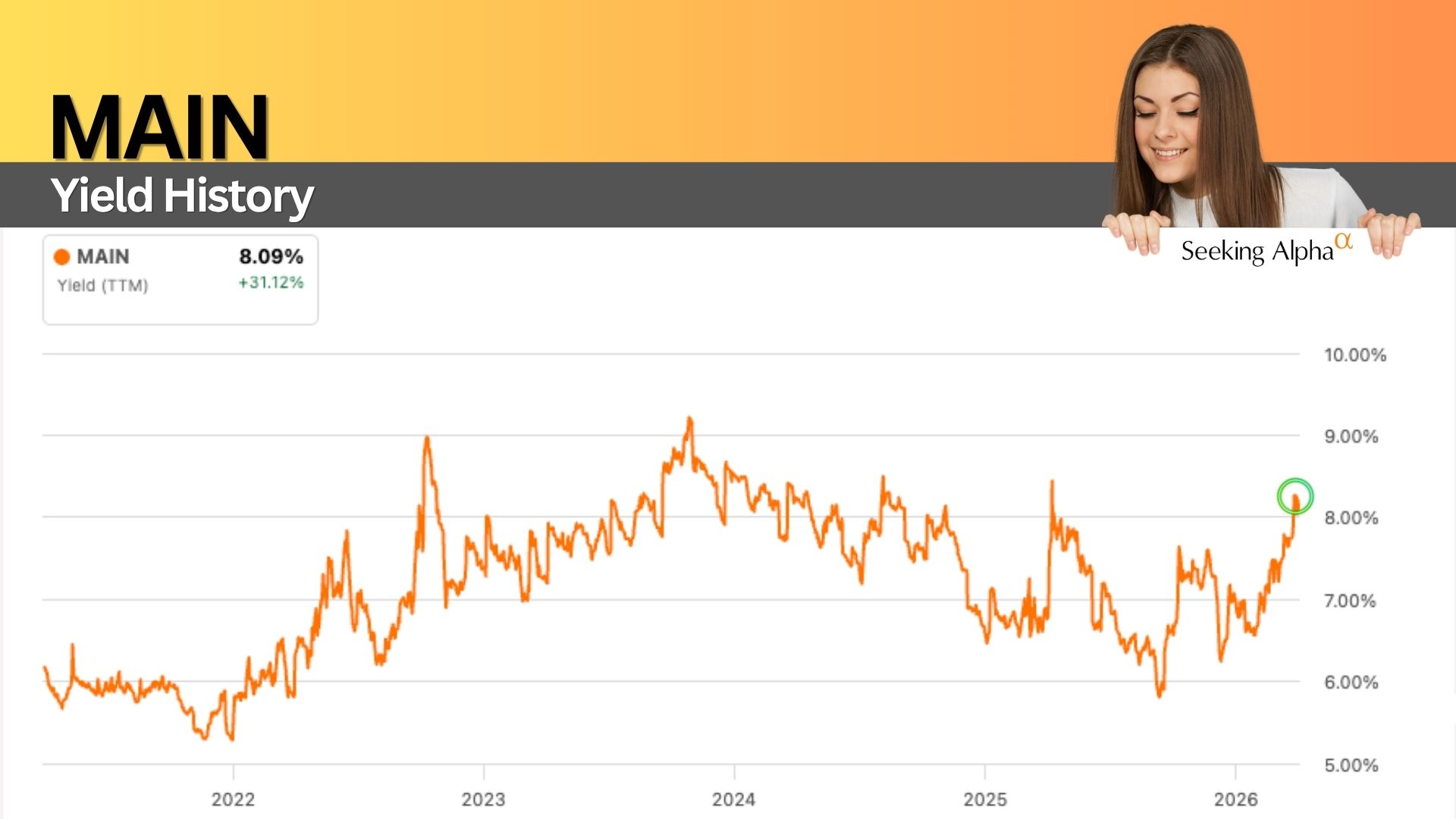

Pricing: The Real Tradeoff

MAIN is almost always expensive.

Even after recent weakness:

It trades above 1.5× NAV

It has one of the lowest yields among BDCs

This is the tradeoff:

you’re not buying the highest yield—you’re buying reliability.

My Take

MAIN offers:

Lower yield than peers

But far more consistent income

And meaningful long-term appreciation

The business remains strong.

The only real question is price.

For me, MAIN becomes attractive at around 1.5× NAV or lower. It’s getting close.

I already have a small position, but if the price dips further, I’ll likely add more.

Final Thoughts

MAIN isn’t designed to maximize yield.

It’s designed to deliver:

Durable income

Strong management execution

Long-term total return

And sometimes, that combination is worth paying for.

To learn more, click here for the full Review.

Want to see how these funds fit into a real-world retirement strategy? I share my full portfolio and monthly updates for free, here: Armchair Insider. If you want to learn from other Income Investors (I do!), check out the Armchair Insider Lounge.