The past month has been a roller coaster. If you don’t enjoy watching your portfolio swing wildly, there are ways to generate consistent income without the drama.

Today we’re looking at a baby bond yielding more than 9%. It doesn’t try to outperform the S&P 500. It simply pays consistent income.

Some investors think that’s boring. I think it’s excellent.

What Is a Baby Bond?

Traditional corporate bonds are designed for institutions. Minimum purchases can run into the thousands of dollars, and they don’t trade like stocks.

Baby bonds are different. They usually issue at $25 per share and trade on stock exchanges using ticker symbols, just like common stocks. That makes them accessible and easier to diversify for individual investors.

ADAMH is one of these exchange-traded senior notes.

Distribution: Fully Defined

Normally I’d hesitate to review something with only one distribution on record. But this is a bond. There’s no discretion about raises or cuts.

We already know exactly what the payments will be.

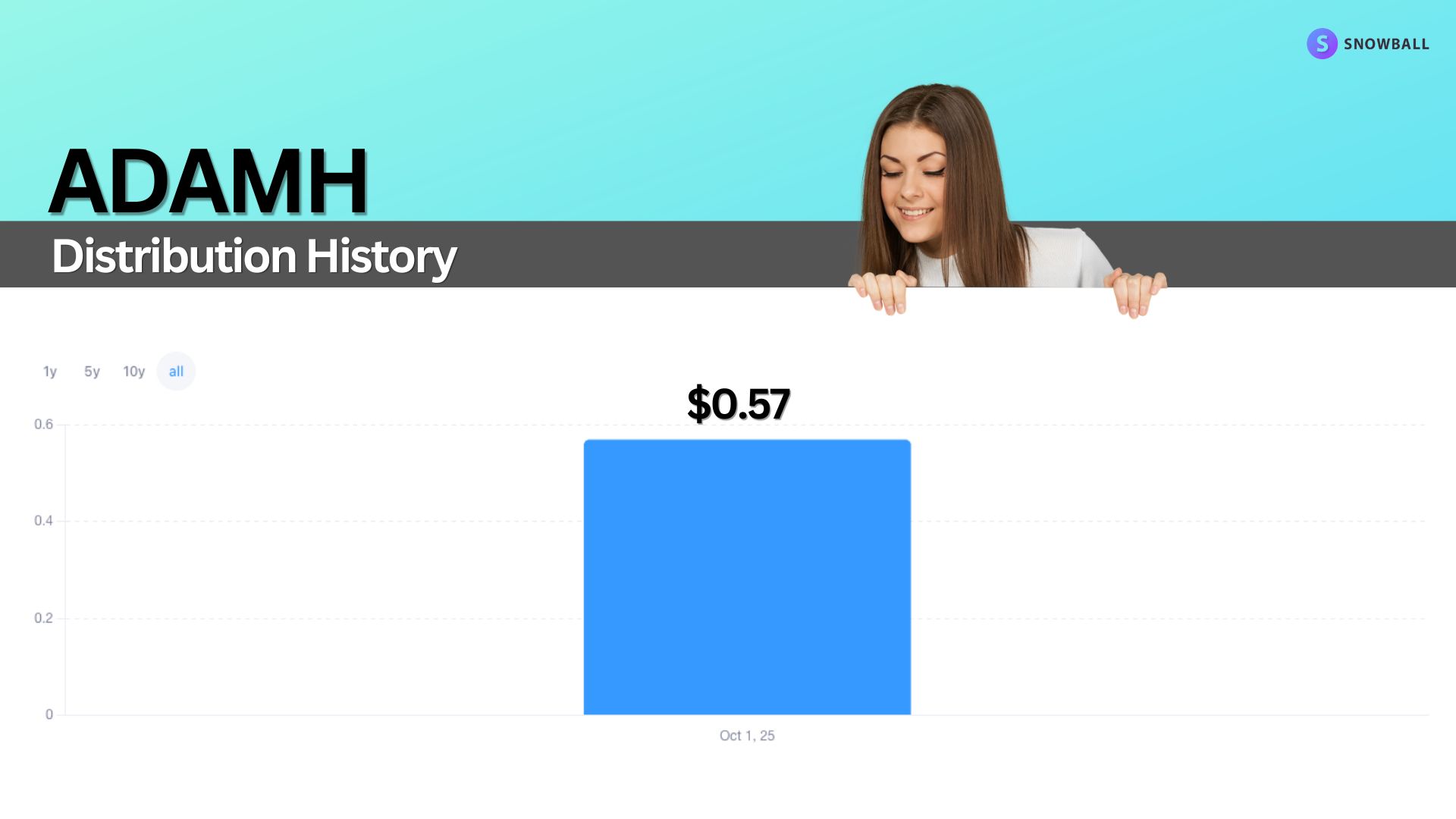

ADAMH pays $2.46875 per year, or $0.6167 per quarter, on January 1, April 1, July 1, and October 1 through October 2030. The first payout was $0.57 because the bond was issued shortly before its first payment date.

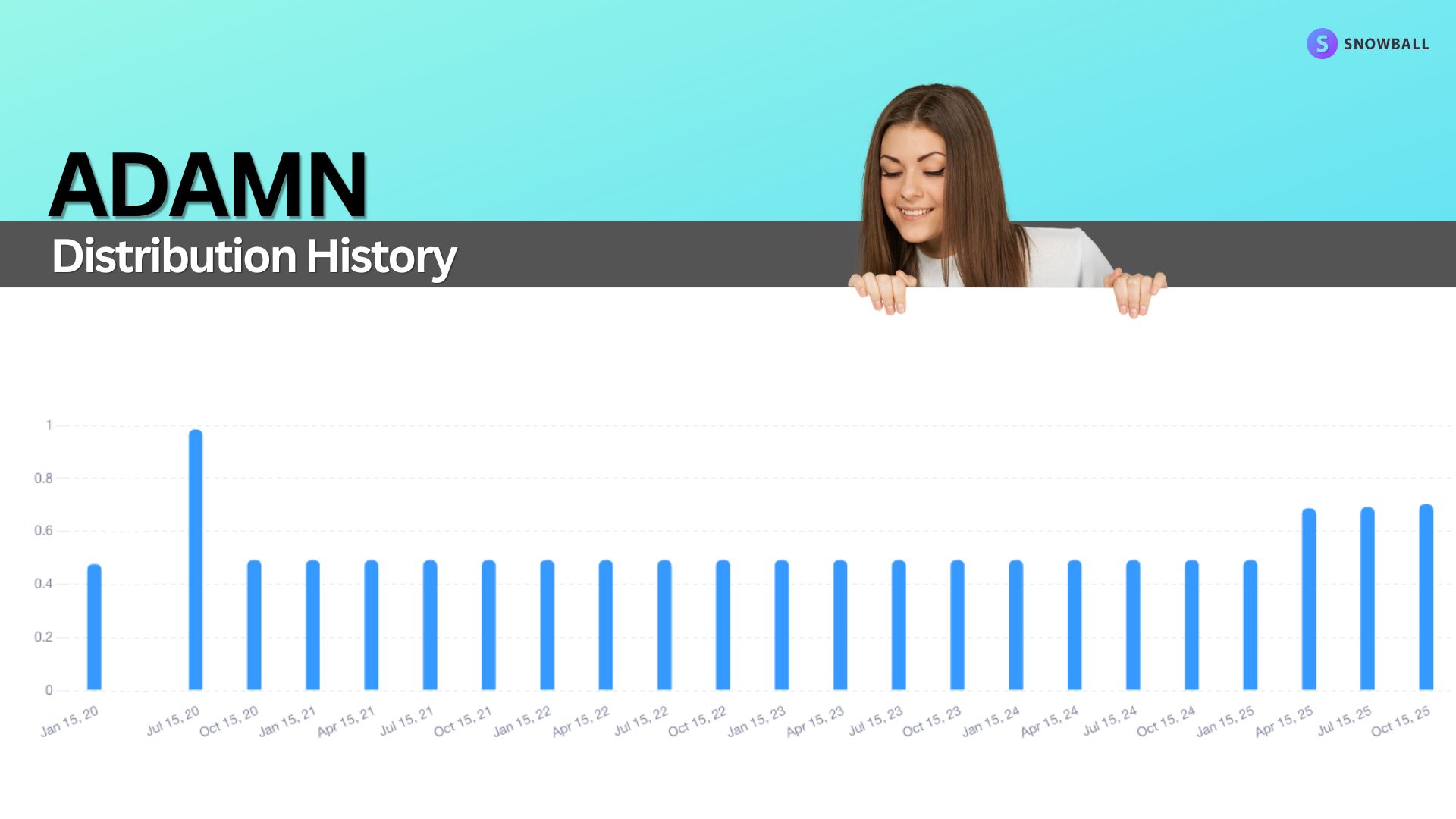

If you want context, look at ADAMI, an older Adamas baby bond.

During the tariff-driven correction, ADAMI declined only modestly while the S&P 500 fell much more. I would expect ADAMH to behave similarly.

Where It Sits in the Capital Structure

ADAMH is a 9.875% senior note due October 2030.

It matures in 2030 and can be called at $25 starting in 2027. Interest payments are fixed, and distributions are taxed as ordinary income. Most importantly, bondholders sit above preferred and common shareholders in the capital structure.

Preferred vs. Bond

Adamas also offers preferred shares such as ADAMN, yielding around 9%.

Preferreds offer similar yield but more risk. If financial stress occurs, bondholders are paid before preferred shareholders. For me, that priority matters.

The Business Behind It

Adamas Trust is a mortgage REIT that invests primarily in residential mortgage-backed securities. Many of these loans are agency-backed, meaning government-sponsored enterprises stand behind the credit risk.

Mortgage REITs are cyclical, which is why I avoid the common shares despite their higher yield. As a lender through ADAMH, my focus is durability and repayment, not growth.

My Take

ADAMH offers the most predictable income and the lowest position in the risk hierarchy.

It won’t double. It won’t crash dramatically. It should consistently pay until 2030.

To learn more, click here for the full Review.

Want to see how these funds fit into a real-world retirement strategy? I share my full portfolio and monthly updates for free, here: Armchair Insider. If you want to learn from other Income Investors (I do!), check out the Armchair Insider Lounge.