In the market landscape of 2026, the traditional comfort of the price-to-earnings (P/E) ratio has become financial archeology. As generative AI and autonomous agents restructure the cost foundations of entire industries overnight, relying on trailing twelve-month data is no longer a conservative strategy.

it is a dangerous form of speculation. For the sophisticated investor, the era of "Relative Valuation" (comparing a stock to its peers) is over, as disruption now occurs at a pace that renders historical benchmarks obsolete. Navigating this volatility requires a shift toward "Absolute Valuation," where the only defensive posture is a rigorous, mathematically sound calculation of a company’s future cash flows discounted to the present.

The Fallacy of the Peer Group: When Homogenization Becomes a Trap

In traditional finance, Relative Valuation is the standard operating procedure. Analysts typically build a peer group of comparable companies, calculate a mean P/E or EV/EBITDA multiple, and determine if a stock is "cheap" relative to its sector. However, in a 2026 generative economy, this methodology is fundamentally broken. Disruption is no longer symmetrical; one company in a sector may be aggressively implementing agentic workflows to slash OpEx by 40%, while its neighbor remains tethered to legacy labor structures.

When you value a stock based on its peer group, you are assuming the "sector average" is a safe harbor. But if the entire sector is facing a systemic decline in its moat, comparing one dying giant to another only yields a distorted margin of safety. This creates a "Value Trap" where a stock appears cheap on paper but is actually a falling knife in terms of its future earnings power.

Moving from Relative to Absolute: The DCF Mandate

To escape the trap of peer-group homogenization, the sophisticated investor must move toward Absolute Valuation. This shift requires treating every investment as a standalone business venture. Instead of asking, "Is this stock cheaper than its competitor?", you must ask: "Does the current price justify the risk-adjusted cash flows this business will produce over the next decade?"

This is where the math of the Discounted Cash Flow (DCF) model becomes the only reliable compass. By focusing on idiosyncratic risk—the risks specific to that company's ability to generate cash—you strip away market noise and peer-group bias.

The Reality Check: In a market saturated with "comparable" data, true alpha is found in the non-comparable. Calculating a company's "floor" price requires a rigorous approach to Intrinsic Value that a simple sector-wide multiple cannot provide.

The Anatomy of a Modern Valuation

The process of determining a company's worth in 2026 involves three high-stakes variables:

Stage-One Growth: The immediate impact of AI integration on margins and revenue scalability.

The Terminal Rate: A realistic assessment of the company’s long-term sustainability in a hyper-competitive environment.

The Equity Risk Premium: Adjusting for the increased volatility of the generative era.

Because these variables are now more sensitive than ever, a minor error in your growth assumption can lead to a massive miscalculation of value. This complexity is precisely why professional-grade tools are mandatory; you cannot accurately run these simulations on the back of a napkin. To maintain quantitative discipline, investors are increasingly turning to a sophisticated intrinsic value calculator to stress-test their assumptions against various disruption scenarios.

Precision in Chaos: Quantifying the Margin of Safety

In an environment where market sentiment can shift based on a single AI breakthrough or a regulatory pivot, "intuition" is a liability. To achieve true defensive positioning, the modern investor must quantify the Margin of Safety—the gap between a stock's market price and its mathematically derived value.

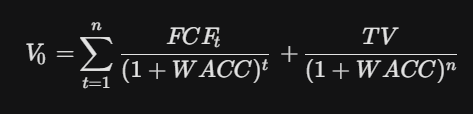

In 2026, this calculation is centered on the Discounted Cash Flow (DCF) model, which serves as the ultimate arbiter of truth. By projecting a company’s Free Cash Flow (FCF) and discounting it by a rate that reflects the heightened risks of the generative era, we can arrive at a valuation that is independent of market hysteria.

The fundamental equation for this absolute valuation is rendered as:

Where:

$V_0$: The current intrinsic value of the business.

$FCF_t$: The projected Free Cash Flow for year $t$.

$WACC$: The Weighted Average Cost of Capital, adjusted for the 2026 Equity Risk Premium.

$TV$: The Terminal Value, representing the business's worth beyond the projection period.

The Sensitivity Mandate: Stress-Testing the Future

The challenge in 2026 isn't just running the numbers; it's accounting for the variance. Traditional DCF models are often criticized for being "garbage in, garbage out." If your growth assumption is off by a mere 0.5%, your valuation can swing by 15% or more.

In a world of agentic disruption, your valuation cannot be a single static number. It must be a probability distribution. This requires Sensitivity Analysis—simulating dozens of scenarios where labor costs, hardware expenditures, and competitive moats shift simultaneously.

Running these high-iteration simulations manually is nearly impossible for the individual investor. This is where the gap between the "retail" and "institutional" experience has historically been the widest. To close this gap and maintain quantitative rigor, utilizing a professional-grade intrinsic value calculator is no longer optional. It is the only way to visualize how a company's "fair value" reacts to different disruption velocities, allowing you to buy when the market prices in a "worst-case" scenario that your data suggests is unlikely.

Terminal Value and the "Moat Erosion" Factor

The most dangerous variable in 2026 valuation is the Terminal Value (TV). Historically, investors assumed a perpetual growth rate of 2-3%. However, as AI lowers the barriers to entry in software and services, the "perpetual moat" is a vanishing concept.

When calculating the Intrinsic Value, we must now apply a "Moat Erosion" discount to the terminal phase. If a company cannot prove it has a proprietary data advantage or a deeply entrenched network effect, its terminal growth rate should be modeled closer to zero—or even negative.

By demanding a higher Margin of Safety on the terminal value, you protect your capital from the "Value Traps" of the generative age. You aren't just buying a company; you are buying a series of cash flows that have been stress-tested against the most volatile economic transition in human history.

The Qualitative Overlay: Evaluating Moats in the Age of Agents

While a robust intrinsic value calculator provides the mathematical "floor" for an investment, those numbers are only as reliable as the competitive moat protecting them. In 2026, the very definition of a "moat" has undergone a radical transformation. Traditional advantages—such as massive physical scale or legacy brand recognition—are increasingly being bypassed by nimble, AI-native competitors that operate with a fraction of the overhead.

To ensure that the cash flow projections in your DCF aren't just "wishful thinking," you must evaluate a company through the lens of Agentic Moats. In a world where AI agents can replicate software features in days, true defensibility now comes from three specific areas:

Proprietary Data Flywheels: Does the company own a unique, non-public dataset that makes their autonomous agents significantly more effective than a generic "off-the-shelf" model?

High-Friction Ecosystems: Is the company’s infrastructure so deeply embedded in a customer’s mission-critical workflow that the "switching cost" remains high, even if a cheaper AI alternative exists?

The Human Trust Premium: In an economy saturated with synthetic content and automated interactions, companies that provide high-trust, human-verified services or physical-world ubiquity are maintaining a premium that pure-play digital companies are losing.

If a company cannot check at least one of these boxes, its intrinsic value is likely much lower than its current earnings would suggest, as its "Terminal Value" is at high risk of a sudden, sharp contraction.

Conclusion: The Synthesis of Art and Science

Investing in 2026 is no longer a choice between "Growth" and "Value." It is a synthesis of qualitative judgment and quantitative discipline. You identify the competitive moat with your insight, but you must define the entry price with your math.

The market remains a "voting machine" in the short term—often driven by AI-fueled momentum and algorithmic noise—but it remains a "weighing machine" in the long term. By shifting your focus from the ticker price to the intrinsic value, you transition from being a speculator to being a true owner of cash-producing assets.

In an era of infinite disruption, your only true protection is the Margin of Safety. Use the math to build the floor, use your judgment to evaluate the ceiling, and never mistake the market's price for the business's worth. Those who maintain this discipline will find that volatility isn't a risk—it's the greatest source of opportunity the generative age has to offer.