My financial life didn't transform because of a market tip or a lucky stock pick. It changed when I stopped treating money as a matter of opinion and started treating it as a system of inputs and outputs. My portfolio’s growth isn’t a product of genius; it’s the direct result of a few core habits that rewired how I interact with my finances.

These are the three foundational habits that shifted my approach from guessing to knowing;and they can do the same for you.

1. I Started Tracking Every Financial Data Point

1. I Started Tracking Every Financial Data Point

Most investors have a general sense of their portfolio's performance. They know if they are "up" or "down." I decided that wasn't enough. I needed to know exactly where my money was going and how every dollar was performing. I began to track not just my spending, but my entire financial ecosystem.

At first, the process of logging every expense, dividend, and contribution felt granular, almost tedious. But soon, it became empowering. I wasn't just looking at a bank balance; I was analyzing a personal cash flow statement. Patterns emerged from the noise. I could see the direct impact of discretionary spending on my savings rate. I could quantify the drag of high-fee funds on my long-term returns.

What gets measured gets managed. For an investor, this isn't just a business cliché; it's the fundamental principle of portfolio optimization.

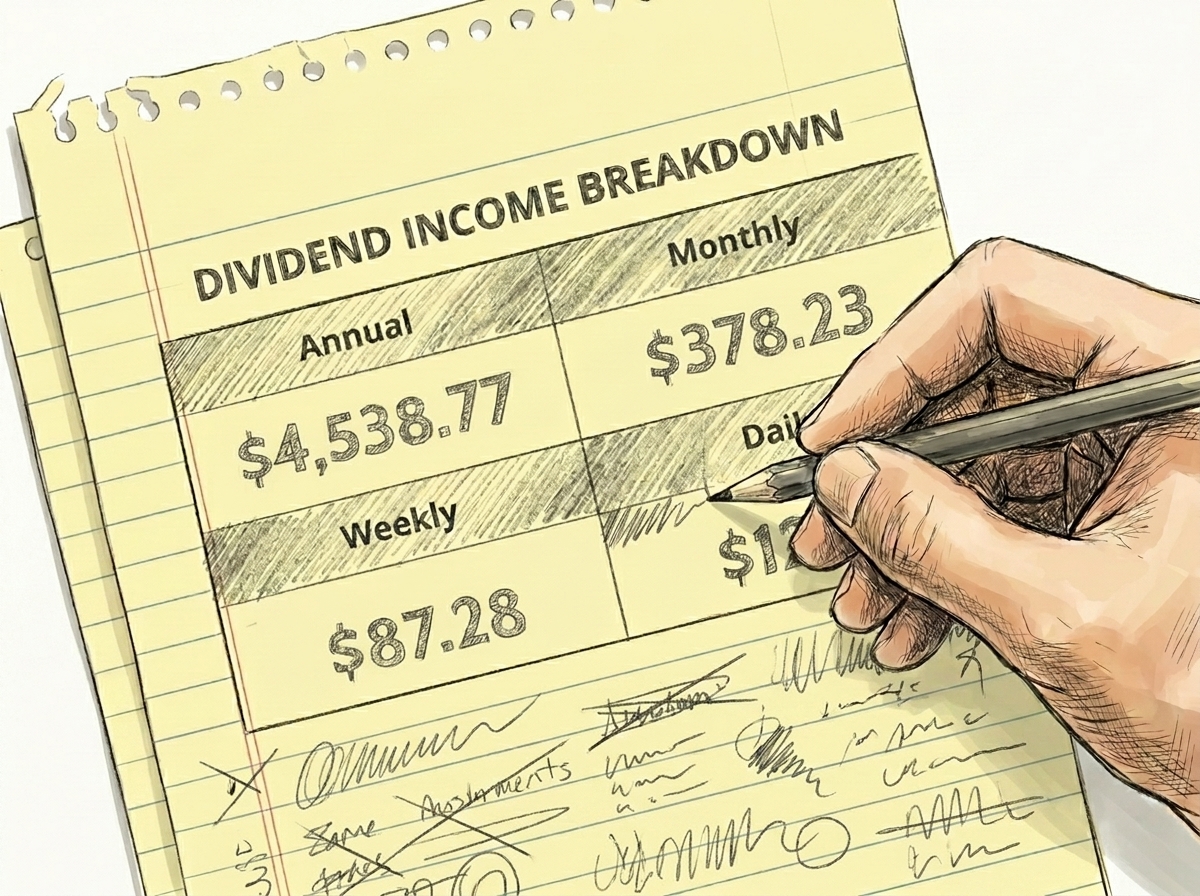

This habit goes beyond a simple budget. It means understanding your personal savings rate, your portfolio's expense ratio, your dividend yield, and your true, time-weighted rate of return. Tools like Snowball Analytics are built on this very principle: that with clear data, you can make better decisions.

If you’re ready to take control of your investments and see your financial picture more clearly, sign up for Snowball Analytics here. You can't optimize what you can't see. Tracking everything is the first step toward gaining that visibility.

2. I Studied the Systems, Not Just the Tickers

2. I Studied the Systems, Not Just the Tickers

Early in my journey, I was obsessed with what to buy. I hunted for hot stocks and chased trends. This approach is exhausting and, more often than not, unprofitable. The real breakthrough came when I shifted my focus from picking winners to understanding the systems that create wealth.

I made it a rule: dedicate time each week to learning about investing frameworks, economic history, and behavioral finance. I didn't need another stock tip; I needed a durable mental model for how markets work. This habit replaced market anxiety with analytical calm. It made building wealth feel like an engineering problem, not a lottery.

Three books were particularly formative in building this analytical mindset:

"The Psychology of Money" by Morgan Housel: It offers a powerful thesis: your behavior with money is more important than how smart you are. It reframed investing as a battle against my own biases, something I could control.

"A Random Walk Down Wall Street" by Burton Malkiel: This classic provided the intellectual foundation for diversification and long-term, index-based investing. It demonstrates, with data, why trying to outsmart the market is often a losing game.

"Thinking, Fast and Slow" by Daniel Kahneman: While not strictly a finance book, this masterpiece on cognitive biases gave me a framework for identifying and mitigating the emotional errors that wreck portfolios.

Studying these systems allows you to build a strategy that is resilient to market noise and your own emotional impulses. It’s the difference between being a passenger, tossed around by market waves, and being the architect of your own financial engine.

3. I Automated My Investment Thesis

3. I Automated My Investment Thesis

Discipline is a finite resource. Relying on willpower to execute your investment strategy month after month is a recipe for failure. The most effective way to ensure consistency is to remove yourself from the day-to-day decision-making process. Automation is the key.

The moment my income hits my bank account, my system takes over:

A predetermined percentage is automatically transferred to my brokerage account.

That capital is then deployed into my target-allocation portfolio of low-cost index funds and ETFs.

All dividends are automatically reinvested (DRIP), harnessing the power of compounding without any active intervention.

I don't have to decide if it's a "good" time to invest. I don't weigh my feelings about recent market performance. The system executes the strategy I designed when I was thinking clearly and analytically. This single shift;from active decision to automated execution;has been the most powerful wealth-building tool in my entire arsenal.

Automation transforms your investment thesis from a plan on paper into a living, breathing machine that works for you. It ensures that you consistently follow the principles of dollar-cost averaging, buying more shares when prices are low and fewer when they are high. It is the practical application of a data-driven strategy.

Final Thought: From Data to Freedom

Building wealth isn’t about discovering a secret. It's about building a superior system. These three habits;tracking your data, understanding the systems, and automating your execution;are the foundational pillars of that system. They are free, simple, and available to you today.

Start with one. Commit to it. The rest of your portfolio will thank you.

Ready to put these habits into action? Explore Snowball Analytics and start your journey today.